CIO Views: UK back in focus; China’s consumer challenge

- 25 Julio 2024 (5 min de lectura)

Chris Iggo, CIO AXA IM Core

UK moves back into investors’ focus

The UK’s economic outlook is improving. Historically, when elections have delivered a change in government with a large majority, both equity and UK bond markets have performed well. The Labour Party’s 174-seat parliamentary majority should mark a period of policy transparency with the stated aim of boosting growth.

The new government has pledged fiscal stability and suggested any new spending will be fully funded, with only selected tax increases as part of the proposed fiscal plans. Partnering with the private sector is also promised, with a focus on energy and other infrastructure projects. As such, the growth-inflation balance should improve, which will support stronger investor confidence in UK assets.

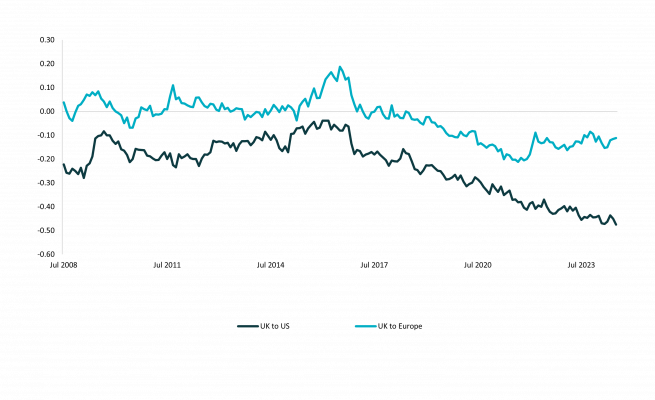

The broad equity market has increasingly traded at a discount to the US and European markets while sterling’s relative cheapness should provide a further attraction to investors and overseas corporates looking to acquire UK assets. In the near term, the Bank of England is likely to start lowering interest rates from their current 5.25% level.

Headline inflation dropped to 2.0% in May and further declines in core inflation should be seen over the second half of 2024. The recent appreciation in the pound’s trade-weighted exchange rate should also help soften inflation going forward. As such, the gilt market and UK corporate bonds are attractive, with shorter maturity investment-grade corporate bonds yielding above 5.0% on average.

Alessandro Tentori, CIO Europe

Bunds in favour

European government bond markets look almost priced to perfection with expectations for a European Central Bank (ECB) deposit facility rate of around 2.70% by the end of 2025 - not far off AXA IM’s forecast. This trajectory is likely to be accompanied by a typical steepening of the German Bund curve, worth around 70 basis points over two years based on the forward curve.

According to ECB President Christine Lagarde, there is a fine line between data dependency and data-point dependency, which will allow the Governing Council to look through unexpected, albeit short-lived, inflation surprises. However, the process of policy normalisation will be subject to uncertainty about the natural rate of interest, i.e. the interest rate at which policy will no longer be deemed restrictive. So what could possibly go wrong for investors?

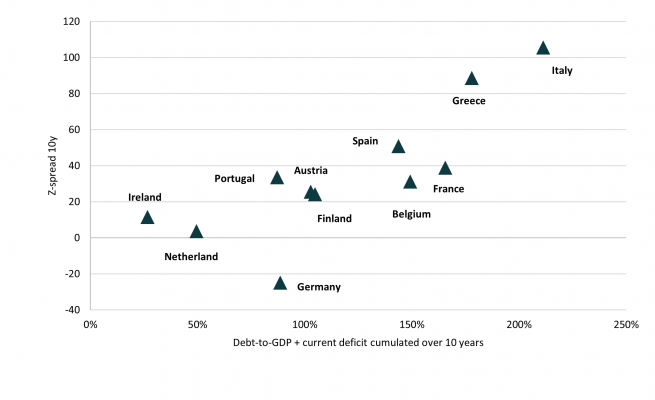

We’ve already had an amuse bouche of government bond volatility in the aftermath of the European Parliament elections. Luckily, this proved to be short-lived. However, it should serve as a reminder of the complex interaction between fiscal and monetary policies. At this stage, European government bond spreads appear to fully reflect differences in fiscal discipline between member states (see figure). However Germany stands out, not only in terms of compliance with the Stability Rules, but also for the valuable liquidity premium attached to Bunds.

Ecaterina Bigos, CIO Asia ex-Japan

More needs to be done for China’s consumer

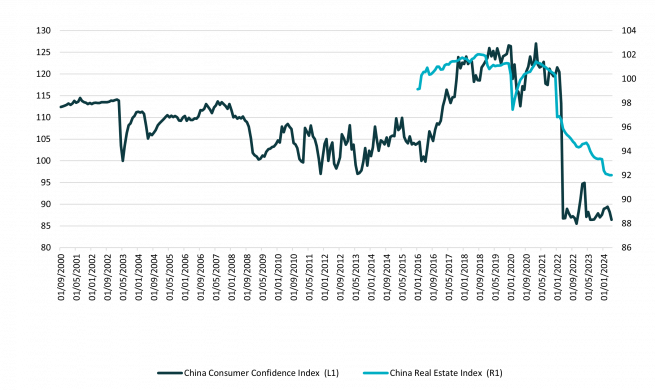

Post pandemic, China has seen positive momentum in fixed asset investment and industrial production. It is also enjoying a revival of export growth in some high value-added sectors. However, China continues to face challenges, as it is looking to rebalance from an investment-led to a consumption-based economy, and it needs to find an alternative to the real estate sector as a lasting source of economic expansion. Its property sector, along with its related activities, once accounted for 25% to 30% of GDP.

Weakness in the sector not only acts as a drag on the overall economy but also on broad consumer confidence, due to its negative impact on wealth. According to a 2019 survey from the country’s central bank, 96% of urban households in China were homeowners, of which nearly 40% owned more than one property.

The government announced various policy packages to support its property market. While the overall direction is geared towards stabilisation and transformation, adjustment is expected to take time. Meanwhile, more needs to be done directly for the consumer, for its transition towards consumption-led growth. Given consumer confidence is very low, policies to expand social safety nets and to grow the middle-income class should be in focus.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

Rates | Data flow in major economies pointing to rate cuts in second half of 2024 | |

|---|---|---|

US Treasuries | Election may impact the timing of a rate cut but Federal Reserve is close to easing | |

Euro – Core Govt. | Further ECB rate cuts expected but markets have priced this in | |

Euro – Peripherals | Bonds remain subject to political events and to the relative debt/GDP outlook | |

UK Gilts | New government pledges fiscal stability. Two interest rate cuts expected this year | |

JGBs | Low returns. Policy indecision by Bank of Japan and weak yen make JGBs unattractive | |

Inflation | Stable expectations as data shows gradually lower inflation in the second half of 2024 |

Credit | Income assets should be part of portfolios. Low spreads suggest limited excess returns | |

|---|---|---|

USD Investment Grade | All in yields are attractive but excess return limited | |

Euro Investment Grade | Stable growth and lower interest rates support income focus in credit | |

GBP Investment Grade | Returns supported, given current yields and expectations of a faster pace of rate cuts | |

USD High Yield | Fundamentals and funding strength remain strong | |

Euro High Yield | Strong fundamentals and ECB cuts support total returns | |

EM Hard Currency | Volatility has subsided but a later Fed interest rate cut will delay recovery |

Equities | Earnings cycle remains robust; AI likely to underpin continued concentrated US returns | ||

|---|---|---|---|

US | Growth set to continue to dominate but need to watch company earnings momentum | ||

Europe | Positive economic surprises and attractive valuations | ||

UK | Monetary policy and change of government should boost sentiment | ||

Japan | Benefits from growth in semiconductors. Reforms in focus for broader performance | ||

China | Growth remains unbalanced. Accelerating industrial output, masks a weak consumer | ||

Investment Themes* | Secular spending on technology, automation, to support relative outperformance | ||

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

CIO team views draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento/ material audiovisual. La información incluida en este documento/ material audiovisual se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.