CIO Views: Markets hold up against volatility spike

- 02 Septiembre 2024 (5 min de lectura)

Chris Iggo, CIO AXA IM Core

August bounce may augur well for rest of 2024

Whatever triggered early August’s volatility spike has not proved serious enough to derail markets’ robust year-to-date performance. Equity and credit markets rebounded quickly while risk indicators – such as the VIX – swiftly reverted to their more benign lower levels. However, the early August moves highlighted that markets are priced to perfection and therefore, vulnerable to adverse fundamental news, even if the volatility was exaggerated by seasonally thin markets. Additional bouts cannot be ruled out in the months ahead given market sensitivity to US labour market data, Japanese monetary policy, and technology company earnings. At the same time, the rapid reversal in the risk sell-off can be seen as good news.

Fundamentals remain supportive. The Federal Reserve should start its interest rate cutting cycle soon - following the moves from other central banks. Elsewhere refinancing problems remain absent in public credit markets while second quarter corporate earnings largely met growth expectations. There has arguably been a moderation in political risk. Strong returns from risk assets might be sustained into the end of 2024, with growth equities and higher beta credit leading the way as they have for the whole of the year. High yield and other short-duration fixed income credit strategies most likely offer the lowest risk path to sustaining positive returns in the final semester of the year.

Alessandro Tentori, CIO Europe

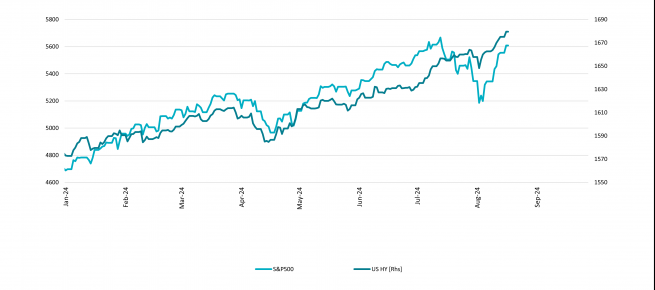

High yield’s optionality opportunity

High-yield bonds are often seen as one of the riskier inhabitants of a portfolio. However, recent stock market volatility tells a different story. The chart compares the Bank of America US High Yield Index with the S&P 500; it shows the market has dropped around 8.5% from 16 July to 5 August, while the US high yield universe actually lost less than 1%. Furthermore, high yield bonds have fully recovered, even reaching new highs for 2024.

There are technical reasons for high yield’s resilience but the point we are making here is related to the ‘defensive option’ embedded in high yield bonds. Just like any corporate bond, they can be decomposed in a risk-free yield and a risky credit spread. This latter component widened roughly 80-85 basis points but the total return effect was somewhat softened by the simultaneous sharp decline in US Treasury yields. Of course, we can compute a break-even between these two components but their inverse correlation is already a beneficial property for bond owners.

The other obvious benefit results from high yield’s rather contained duration, which is especially valuable during periods of relatively high absolute yield. The trade-off here is between credit risk and time value - investors enjoy an attractive carry profile, while at the same time avoid excessive sensitivity to spread widening. Once the US economy avoids recession – and we’re not forecasting one in the near future – investors should potentially reap the benefits.

Ecaterina Bigos, CIO Asia ex-Japan

China’s uphill journey of rebalancing its economy

China’s current economic armoury - infrastructure and manufacturing sector investment – appears to be helpful in defending its real GDP growth. However, it comes with a cost of entrenching deflationary pressures and rising concerns of overcapacity. The downward pressure on the Producer Price Index also affects export prices, which is contributing to the fears of exporting deflation. While this is being tolerated for now, as many countries grapple with high inflation, it could become problematic when inflation rates fall within target ranges.

An exit from deflation, helped by global trade, looks increasingly challenging. The rather notable sequential slowing in July’s exports, with broad-based easing across major developed and emerging markets, is sending tentative signals the export engine may soften. As the export sector has been an important growth driver for China’s economy in recent quarters, amid ongoing weakness in the housing sector and sluggish consumption growth, potential slowing would imply growing uncertainty on the industrial sector's growth outlook going into the second half of 2024.

This comes on the back of cautious signals from the external front of slowing demand. Further out, trade tensions concerns are a major uncertainty. The current stimulus plan, if fully implemented, without changes, may exacerbate the issue of overcapacity, add to disinflationary pressures, and increase the future debt burden.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

Rates | Developed economy data points to interest rate cuts from September - path from there is less certain. | |

|---|---|---|

US Treasuries | Fed likely to ease in September. Volatility remains a risk on new economic data and path from the first cut | |

Euro – Core Govt. | Further ECB rate cuts expected; political uncertainty remains a risk | |

Euro – Peripherals | Presents opportunities and higher real yields than Bunds | |

UK Gilts | Interest rate cuts fully discounted; markets await fiscal plans | |

JGBs | Uncertainty over Bank of Japan policy normalisation path. Yen remains volatile | |

Inflation | Stable expectations, with gradually lower inflation for the rest of 2024 |

Credit | Favourable pricing is increasing the asset class’s contribution to excess returns | |

|---|---|---|

USD Investment Grade | Without significant growth deterioration, credit to remain resilient | |

Euro Investment Grade | Resilient growth and lower interest rates support credit’s income appeal | |

GBP Investment Grade | Returns supported by better growth and expectations of rate cuts | |

USD High Yield | Narrative of growth without inflation is supportive. Fundamentals and funding remain strong | |

Euro High Yield | Strong fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Higher quality universe, well-placed with US interest rate cuts commencing |

Equities | Lower inflation will impact earnings cycle. Unmet return expectations from AI spending is a risk | |

|---|---|---|

US | Growth and quality to continue to dominate - but need to watch company earnings momentum | |

Europe | Attractive valuations, along with positive economic and earnings surprises | |

UK | Relatively more attractive valuations and positive economic momentum | |

Japan | Benefitting from semiconductor growth. Reforms and monetary policy in focus for broader performance | |

China | Growth remains unbalanced. Accelerating industrial output masks a weak consumer | |

Investment Themes* | Secular spending on technology and automation to support relative outperformance |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

CIO team views draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.