China reaction: monetary easing delivered, now waiting for fiscal coordination

- 24 Septiembre 2024 (5 min de lectura)

The PBoC unveiled a series of monetary policy measures following today’s unusual press conference, aimed at supporting the economy as the growth target becomes increasingly elusive. The newly announced package is designed to ease monetary conditions across the broader economy, with a particular focus on the housing market. The measures include reductions in the RRR, policy rate, outstanding mortgage rate, and minimum down payment ratio for second homes. Additionally, the re-lending programme for the housing stock buy-back scheme will be strengthened, and restrictions on the equity market will be loosened. This announcement aligns broadly with expectations, though it leans slightly stronger than anticipated. However, it is unlikely to outweigh the current entrenched economic downturn – coordination from fiscal policy is needed to ensure a good efficacy.

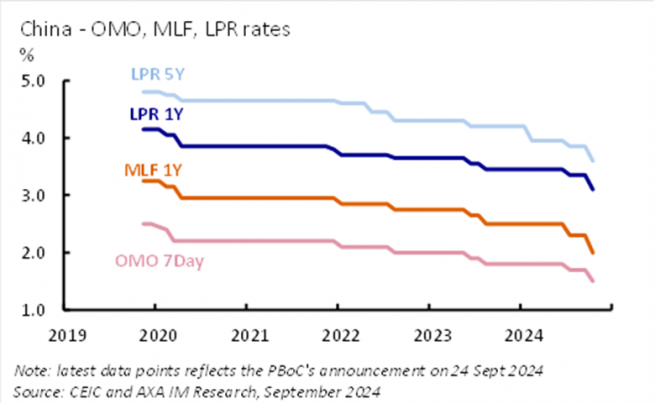

Rate cuts across the board and a special focus on properties

A 50bps reduction in the RRR, which applies to mid-sized and large banks, was announced, in line with expectations. This will bring the weighted average RRR down from 7.0% to 6.6%. The PBoC also promised an additional unexpected RRR cut of 20-50bps by the end of the year. The 50bps reduction will release 1 trillion Chinese Yuan (RMB) in long-term liquidity into the banking system, and further cuts in the coming months will continue to provide liquidity support to banks.

The 7-day reverse repo rate will be trimmed by 20bps, to 1.5% from 1.7%, as confirmed by Governor Pan Gongsheng, slightly exceeding expectations. This will result in a 30bps cut to the 1-year medium-term lending facility (MLF) rate to 2.0%, with deposit and Loan Prime Rates (LPR) also expected to drop by 20-25bps. According to Pan, these changes are "neutral" to commercial banks’ net interest margins.

The package includes further support for the property market. Existing mortgage rates will be cut by around 50bps on average, which is slightly more than expected. In addition, the downpayment requirement for second homes will be lowered by 10ppts to 15%. The PBoC has also enhanced the re-lending programme for the housing stock buy-back scheme, increasing the funding support ratio from 60% to 100%. The scheme's quota and rate remain unchanged at RMB 300 billion and 1.75%, respectively. The re-lending programme has been underutilised to date —only 4% of the quota was issued by the end of Q2—the enhanced funding ratio should improve policy execution and help reduce housing inventory.

Monetary easing alone unlikely to revive credit demand

While liquidity injections may help lower borrowing costs, they may not automatically generate credit demand. What is lacking in China’s financial system at the moment is not liquidity but genuine demand for credit. The reduction in mortgage rates in that sense is more welcome by households, but in itself is likely to be too small to restore consumer confidence fully. A persistent interest rate gap between new and existing mortgages, estimated at around 84 bps and this has now been reduced. Today’s rate cuts could save households RMB 150 billion in interest payments—equivalent to 0.3% of annual retail sales—and this boost to incomes may translate to higher spending. However, without a significant improvement in confidence, the saved mortgages from the rate reduction could be translated to increased household savings or another round of prepayments, amid the negative asset price outlook and homeowners concerns about their debt persist.

New instruments to support equity market

The PBoC also announced new measures to support the equity market. Qualified securities firms, funds, and insurance companies will be permitted to use funding from the PBoC to buy stocks through a swap facility. The quota for the first batch is set at RMB 500 billion, with the possibility of increasing it by up to two additional batches, contingent on its effectiveness.

In addition, a specialised re-lending facility for stock buybacks by listed companies and major shareholders will be established, with an initial quota of RMB 300 billion. Notably, this facility will be available to companies across different ownership types, including privately owned enterprises.

Good move, but can be better

While monetary easing is necessary, the scale of measures announced today is unlikely to be sufficient to reverse the current economic weakness given the severe lack of risk appetite and credit demand. The de facto fiscal austerity – with local government actions not reflecting central government ambition - remains the primary drag on growth momentum. A pragmatic rebalancing of responsibilities between central and local governments is essential to ensure smooth policy transmission and break this “austerity trap”.

Following today’s announcement, we maintain our growth forecast for 2024 at 4.8%, with slightly reduced but still present downside risks. A strong, coordinated fiscal policy in the near term is both important and necessary to ensure the effective transmission of today’s monetary easing measures. For 2025, we expect a GDP growth rate of 4.4%.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.