High yield bonds: Will the rebound continue?

- 10 Agosto 2022 (7 min de lectura)

- Fixed income investors have endured a harsh first half to 2022 but we see opportunities emerging in high yield bonds

- In our view valuations are currently attractive and the potential for better returns has improved

- Even if the economic backdrop deteriorates, we believe high yield can weather the uncertainty

The first half of 2022 marked the worst six months for US high yield bonds since the 2008/2009 financial crisis with the market down 14% over the period.1

Investors have been hit by an increase in underlying Treasury yields and a widening of high yield corporate credit spreads. Higher inflation, Federal Reserve monetary tightening and fears of an economic slowdown going into 2023 have been the major macroeconomic narratives. And as things stand, the economic outlook remains uncertain.

But despite all this, we can see the emergence of attractive opportunities in the US high yield market. In our view, the chances of investors potentially seeing positive total returns over the next year have improved given the levels which both absolute yields and credit spreads have reached.

Risk assessment

High yield bonds are viewed as more risky investments than government or investment grade corporate bonds. This is because they tend to be issued by companies with weaker balance sheets, typically with higher levels of leverage, i.e. debt relative to revenue.

The key risk with high yield bonds is of potential default – when the issuing company is unable to meet its contractual coupon or maturity payments. However, their main attraction is the typically higher yield on offer relative to investment grade or government bonds.

When assessing high yield bonds, investors need to consider the absolute yield on offer and how it compares to other asset classes.

While past performance should not be viewed as a guide to future returns, diversified exposure to high yield bonds can potentially deliver positive returns over time. For example, over the past 20 years, the asset class has achieved an annualised return of 7.66% – and 4.8% over 10 years.2 However, rising default risk can contribute to heightened levels of volatility and periods of negative return.

At the end of July 2022, the so-called yield to worst – the measure of the lowest possible yield that can be received on a bond without a bond defaulting – on the ICE BofA US High Yield Index stood at 7.67%, down from a 2022 peak of 8.9%.3

Yields have been higher than this in the past, most recently during the initial COVID-19 shock. They were also higher in 2015-2016 when a fall in global oil prices exposed some highly leveraged energy companies and were also elevated during the global financial crisis. But following each episode, yields fell back sharply in the year following their peak.

Of course, there is a risk that yields go higher again in the months ahead, given the potential for a deterioration in the US economic environment but we believe the outlook is improving.

Spreading risk

The additional yield offered by high yield bonds is there to compensate investors for the higher risk of default or other credit events. High yield bonds have higher spreads – the difference in the yield between two different types of bonds – because of the risk of default compared to investment grade bonds.

Credit ratings indicate different cohorts of risk in the market, with BB-rated bonds better quality (lower default risk) than CCC-rated bonds. Notably, at the end of July the spread of high yield relative to government bonds was at 312 basis points (bps) for BB-rated bonds, and 1,092 basis points for those rated CCC and below.4

For the overall high yield index, the spread stood at 477 basis points at the end of July.5 Spreads have been wider during the periods of market stress.

Indeed, the absolute yield looks to be at more of an extreme relative to the level of spread because risk-free rates have recently risen to levels not seen since before the financial crisis in 2007.

Taking month-end index data since the end of 1996, if the option-adjusted spread on the index was above the end-July 2022 level of 477 bps, the subsequent 12-month excess return relative to government bonds was positive 64% of the time, according to our own analysis. We also found when the yield-to-worst has been above the end-July 2022 level of 7.67%, the subsequent 12-month total return has been positive 79% of the time.6

For the BB-rated cohort, the positive outcomes happened 68% and 87% of the time when the spread and yield were at or higher than the end-July levels. When the holding period is extended to 24 months, at the overall index level, when the entry point has been with the option-adjusted spread above 477 bps, positive excess returns occurred 77% of the time.7

Market value

If valuations are currently attractive, where does this leave fundamentals? The macro outlook is hardly covered in glory; growth is expected to slow, and some economists are warning of a possible recession in late 2022 or 2023. Historically, spreads have widened going into a recession and peaked during the recessionary period.

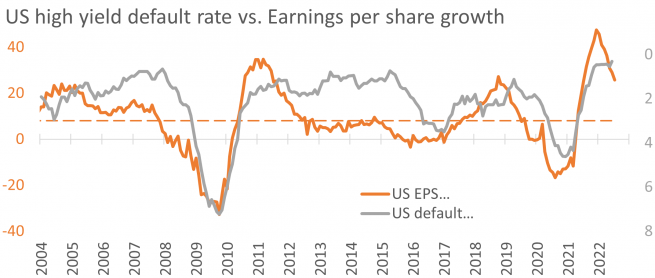

The widening of spreads has anticipated a rise in defaults in the high yield market. Since the 2008 crisis, the default rate in the high yield index has averaged 1.9%. Since 2015, a period that includes the energy and COVID-19-related default cycles – which peaked at 3.5% and 4.6% respectively – the default rate in the same index has averaged some 2.2% at the mid-year mark.8

Defaults have been very low in recent years on the back of the previously more benign economic backdrop of low interest rates and market liquidity. Additionally, companies have generally managed their balance sheets and debt better. However, we expect default rates to increase in the next year or so as the US economy slows.

Our quantitative default model indicates a default rate of 2.3% over a year, above the average of recent years but below recent default peaks. By comparison this forecast stood at less than 1% between January and the end of February and under 2% until the end of April.9

What is key, however, is that the market repricing has also pushed spread-implied default rates higher. At the end of July, the index had a spread-implied default rate of 3.4% – down from 4.2% over a month.10 That is comfortably above our model forecast of 2.3%, which we still believe makes the market cheap from a default valuation perspective.

Idiosyncratic-driven defaults

Given this current environment we expect any increase in defaults to be driven by idiosyncratic, company-specific reasons rather than something systemic or sector-specific. There are already indications from the bond market that interest rate expectations have peaked. If this is the case it will help limit the extent to which economy-wide credit conditions deteriorate.

Of course, borrowing costs for companies have risen. The average coupon on existing debt in the high yield market was 5.73% at the end of July while the yield-to-worst is 7.67%.11 If a company needs to refinance debt now it will have to pay a much higher coupon, which threatens a rise in defaults if cashflows are not strong enough to meet those additional interest payments or if investors aren’t willing to finance debt at higher coupons.

Indeed, for the current cohort of the index, if current market pricing was to persist over the six-year weighted-average life of the index, it would add around 5.5% in debt cost annually.12 This is a material increase that could erode balance sheet health if corporate earnings fall but it could broadly be manageable if average earnings growth was at 10% plus.

The good news is that there is no material wall of refinancing coming. In our view, companies in the high yield market are entering this period of economic uncertainty in a relatively healthy financial state. At the mid-year mark there was around $50bn of high yield debt maturing in the next year, representing just 3% of the total high yield market.13

- Qmxvb21iZXJnLyBJQ0UgQm9mQSBVUyBIaWdoIFlpZWxkIEluZGV4IGFzIGF0IGVuZCBKdW5lIDIwMjI=

- Qmxvb21iZXJnLCBhcyBhdCB0aGUgZW5kIG9mIEp1bHkgMjAyMg==

- Qmxvb21iZXJnIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyBhdCBlbmQgSnVseSAyMDIy

- Qmxvb21iZXJnIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyBhdCBlbmQgSnVseSAyMDIy

- Qmxvb21iZXJnIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyBhdCBlbmQgSnVseSAyMDIyIA==

- QVhBIElNIGFuYWx5c2lzIEp1bHkgMjAyMg==

- Qmxvb21iZXJnIC8gQVhBIElNIGFzIGF0IGVuZCBKdWx5IDIwMjI=

- SUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyAzMCBKdW5l

- SUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCAvIEFYQSBJTSA=

- QVhBIElNIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyBhdCBlbmQgSnVseSAyMDIy

- Qmxvb21iZXJnIC8gQVhBIElNIGFzIGF0IGVuZCBKdWx5IDIwMjI=

- SUNFIEJvZkEgLyBBWEEgSU0gYW5hbHlzaXM=

- QVhBIElNIEp1bmUgMjAyMiAvIElDRSBCb2ZB

Average pricing

This brings us to another aspect of the current high yield market. Due to a long period of low interest rates, the rise in yields in the last year has pushed the dollar price of bonds down. The par-weighted price for the index altogether is 90.4 cents.14

In the 25-year history of the ICE BofA US High Yield Bond Index, the average price has only been lower on four other occasions – briefly during COVID-19, end-2015, the 2008/2009 crisis and in the wake of the dot.com bust in the early 2000s. The pull-to-par should ensure, even with a rise in defaults, a double-digit move in the current average price of bonds as they reach maturity over the next few years.

The opportunity provided by current pricing in the US high yield market is defined by low average dollar prices, yields and spreads at levels that have historically provided a high probability of above-average returns, and a better potential risk-adjusted return relative to other fixed income assets.

We look at how much yields and spreads would need to increase from today’s levels for a purchase of a high yield basket to break-even. For the US high yield market this would be a further 1.85% of yield to get a zero total return or a 113 bps increase in spread for the excess return relative to government bonds to be zero.15

That is quite a cushion and compares very favourably with US investment grade bonds and emerging market bonds. European high yield also has elevated break-even rates albeit with a worse macroeconomic backdrop.

Echoing equities

High yield represents an exposure to corporate cashflow and is thus somewhat cyclical and correlated to returns in equity markets. Historically excess returns in the high yield market have been broadly comparable to equities. What happens to the US equity market is a consideration in potential US high yield returns. Investors looking for an upturn in corporate asset valuations could potentially consider high yield bonds relative to the equity market at this stage.

Given the above arguments, we believe, there appears to be less downside risk to high yield returns compared to equities, given that valuations in some parts of the equity market remain well above previous recession-like levels.

Historically, high yield returns have been considerably less volatile than equity returns, accruing around 42% of upside returns of the equity market and around 35% of downside returns.16 It is important to keep in mind that at the individual issuer level, if companies are listed, they will halt dividend payments to shareholders before coupon payments to creditors are interrupted.

Finally, we would also argue that we believe fixed income generally, and high yield particularly, is better placed to contribute positively to the performance of multi-asset portfolios. Yields have risen and are unlikely to fall back to the very low levels that prevailed during the 2021 period.

Income from bonds is likely to now play a more important role in portfolio total returns while the rise in underlying risk-free rates potentially provides more of a natural hedge against the riskier components of a multi-asset portfolio.

- Qmxvb21iZXJnIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBJbmRleCBhcyBhdCBlbmQgb2YgSnVseSAyMDIy

- Qmxvb21iZXJnIC8gSUNFIEJvZkEgVVMgSGlnaCBZaWVsZCBCb25kIEluZGV4OyBBWEEgSU0gY2FsY3VsYXRpb25zIGFzIGF0IGVuZCBvZiBKdWx5IDIwMjI=

- UmVmaW5pdGl2IERhdGFzdHJlYW07IEFYQSBJTSBjYWxjdWxhdGlvbnM7IGVuZC1KdWx5IDIwMjI=

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.