UK Budget reaction: Going for growth

- 31 Octubre 2024 (5 min de lectura)

Going for growth

The new Labour government campaigned on a platform of economic change to “kickstart economic growth”. In her first Budget, Chancellor Rachel Reeves delivered a host of changes that took her over an hour and a quarter to deliver – and plenty more time to digest. The Chancellor made good on repeated warnings that taxes would rise, she announced tax hikes that are forecast to sum to £36bn/year – 1.1% of GDP. However, she avoided breaking any manifesto pledges with tax increases coming in the main to Employers’ national insurance, but included capital taxes and a scrapping of the non-domiciled residents tax scheme.

Reeves explained that the tax increases were to fix the £22bn “hole in the public finances” and to make sure that the new government would not follow the previous government’s austerity. This was certainly the case, with Reeves setting out an average £70bn increase in spending over the coming five years, mainly supporting day-to-day expenditure in education and health, but with a broad swathe of other measures and including increases in investment spending.

With the discrepancy between tax and spending measures, borrowing increased sharply. Public sector net borrowing is now forecast £140bn higher over the coming five years than before – although Reeves warned that this comparison was not complete and net debt is now seen at 97.3% in 2028-9 (3ppt higher than in March). However, Reeves also introduced a more fundamental overhaul of the fiscal rules. She shifted the focus to constrain day-to-day spending, requiring a current budget surplus by 2029-30, and ultimately three years out, while shifting the focus from public sector net debt to public sector net financial liabilities – a metric that captures the assets that the public sector will invest in, not just the liabilities.

This allows for a boost to spending and investment in the UK economy, something that the Office for Budget Responsibility (OBR) thinks will underpin a rise in growth to 2.0% next year and 1.8% next, closing the output gap earlier than previously expected and bolstering trend growth (if sustained) over a longer time frame (in newly proposed 2030 onwards forecasts). We ourselves consider the growth forecasts the OBR has presented as optimistic. At the same time we see the net loosening in the headline fiscal stance – albeit acknowledging the Chancellor’s concerns around a straight comparison – as something that is not going to prompt the Bank of England to quicken the pace of easing from its implicit sub-4% by end-2025 assessment from August, forecasting Bank Rate at 3.75% by end-2025 .

Market reaction was measured. Gilt yields rose notably, impacted both by the change in supply outlook and a revision to the balance of risks around the BoE’s rate outlook. But broader markets gave the new Chancellor the benefit of the doubt, sterling rising versus the US dollar (compared to the ignominious collapse in 2022) and a modest boost to domestic equity markets.

Measures – chunky tax increases, but even more spending

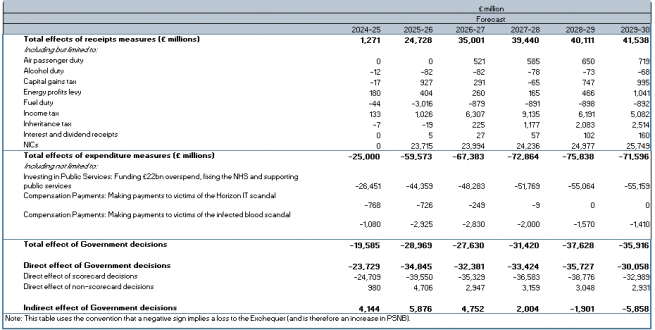

Today’s Budget lived up to expectations of setting out the new government’s stall, delivering significant changes on both the tax and spending front. The OBR outlined a £25bn increase in spending this year and an average of £69.5bn in each of the following five years, equivalent to a 2.2% of GDP increase per year. Tax revenues, meanwhile, are forecast to increase by around £36.2bn a year, equivalent to 1.1% of GDP.

On the spending side, the main measures focused on departmental spending. Around two-thirds of the increase in spending is due to go towards day-to-day budgets and just under a third to capital spending, according to the OBR, with the NHS and education sectors set to benefit the most. The incoming government also set aside funds to reimburse those affected by the infected blood and Post Office horizon scandals, amounting to £2.3bn a year over the forecast horizon. Meanwhile, tightening eligibility for winter fuel payments is estimated to save the government £1.6bn a year.

To fund (some of) this increase in spending the government made good on its threats of tax increases. The OBR estimates that Chancellor Reeves’ tax changes will raise an additional £36.2bn a year on average from FY25/26 onwards, pushing up the tax burden to 38.2% of GDP by the end of the forecast horizon, 5.1pp higher than on the eve of the pandemic. Notable changes included the 1.2pp increase in NICs to 15%, from 13.8%, which looks set to generate £24.5bn a year from FY25/26 onwards and changes to capital taxes which are estimated to raise an average of £5.6bn a year in total. Within that, changes to capital gains tax – including hiking the lower rate to 18%, from 10%, and the higher rate to 24%, from 20% - looks set to generate £1.7bn, while changes to inheritance tax, including closing loopholes on business and agricultural estates and including pensions will generate £1.1bn each year. Further changes to the so-called non-dom scheme, meanwhile, look set to generate around £2.5bn. Finally, the removal of VAT exemption for private school fees from January will raise £1.6bn a year from 2025.

However, the discrepancy between expected tax revenues and spending already suggests an increased burden on borrowing. Moreover, the OBR notes high levels of uncertainty around some of its expectations on revenue and costings, given the unknown behavioural response to some measures. For instance, individuals may change the timing of asset disposals or transactions in response to changes to capital taxes. They also may shift between different assets to take advantage of differences in effective tax rates, plan their taxes more effectively to reduce the effective tax band through the use of reliefs, gilts or vehicles with more favorable tax treatment or simply divert activity to countries where the tax liability is lower. The infected blood and post office scandals may also end up costing more.

The public finances – fiscal rules shift focus, but borrowing still higher

The public finances have moved significantly compared to last March. Chancellor Reeves was clear to point out that the inclusion of “undisclosed” metrics now compared to last March would have made, what the OBR described as a “material difference” to projections in March. This means that a comparison of this first Labour Budget with the position as stated in March does not signify the sum total of the new Chancellor’s measures.

The Chancellor took the opportunity of her first Budget to introduce a new set of fiscal rules.

- To see the current budget (deficit excluding investment) in surplus by 2029-30, until 2029-30 becomes the third year of the forecast, when it will become a rolling third year target. At present the OBR forecasts a current budget surplus of £10.9bn in 2027-28.

- To replace public sector net debt with public sector net financial liabilities (PSNFL) and to see that fall as a % of GDP by 2029-30 until 2029-30 becomes the third year of the forecast, when it will become a rolling third year target. At present the OBR forecasts PSNFL to be fall from 2026-27 onwards..

- Reeves maintained the previous target that welfare spending should remain within a predetermined cap and margin in 2029-30.

The Chancellor also announced further changes to the fiscal Charter, including the introduction of a fiscal lock, requiring the OBR to scrutinize tax or spend changes in excess of 1% of GDP; increased transparency with regards to a wider range of departmental spending pressures; a commitment to regular spending reviews of three years outlook every two years; and a commitment to hold only one major fiscal event a year, barring an economic shock.

However, the plain comparison between the state of the UK public finances now and in March has deteriorated materially – and the new government’s actions – in spending more than they have increased taxation – has added to that deterioration. In old money, public sector net borrowing is estimated to 4.5% of GDP again in 2024-5 – the same as last year – up from a forecast 3.1% in March, falling to 3.6% in 2025-6, 2.9% in 2026-7, then 2.3%, 2.2% and 2.1% in subsequent years. Borrowing over the five years including this is now forecast £142bn higher, around 5% of GDP. The deficit as a percentage of GDP is forecast to be 1.4ppt higher than forecast in March for this year, 0.9ppt next, then 0.6ppt, 0.6ppt and 1.0ppt.

This is also evident in terms of public sector net debt, which although estimated to total 98.4% this year (compared to 98.8% in March), it is set to fall much more slowly than previously expected to now reach 97.3% in 2028-9, compared with the previous March forecast of 94.3% (95.6% vs 92.9% excluding BoE). The previous fiscal rules, which necessitated debt to be falling as a percent of GDP by the fifth year of the forecast, had provided scant constraint to previous Chancellor’s as they only required debt to decline between year four and five. We are not particularly concerned that this would not be met under the current projections. However, the fact that overall borrowing is so much higher is more concerning. At this stage, the Chancellor explains that the transition to PSNFL allows for worthwhile investment to be undertaken and to consider the assets of such investment, not just the liabilities. However, the risk of rising liabilities persists, not least as we consider the OBR’s growth outlook for the coming years optimistic, despite today’s announcements, with any shortfall in growth likely to weigh on tax revenues and further lift borrowing.

The economy – set to revive, but how quickly ?

On the economic front, Chancellor Reeves set out to deliver a Budget that would boost growth over the longer term and on that front she has delivered… just. In the very near term, the net fiscal easing looks set to boost growth, with the OBR revising up its 2024 forecast to 1.1% - in line with our own – from 0.8% previously and its 2025 forecast by 0.1pp to 2%. Admittedly, over the latter part of the forecast horizon, the OBR expects some crowding out of private activity in an economy with little supply capacity to weigh on growth in the final years of the outlook period, while the increase in employer NICs is expected to reduce labour supply by 50K average hours.

As a result, the OBR revised down its growth forecasts for 2026 to 2%, from 1.8%, 2027 to 1.5%, from 1.8% and 2028 to 1.5%, from 1.7%. The big picture, though, is that from the OBR’s perspective at least, today’s budget leaves the level of GDP broadly unchanged at the five-year forecast horizon, compared to the previous budget and is positive for growth over the longer term if the increase in public investment were to be sustained, given the boost to capital stock and potential output.

We doubt economic activity will recover that quickly over the next couple of years, however, leaving the level of GDP weaker than the OBR currently expect at the end of the five-year forecast window. Yes, our forecast for Bank Rate to fall by 25bp a quarter over until midway through 2026 – leaving it at 4.75% by end-2024, 3.75% by end-2025 and 3.25% by end-26 – is slightly more aggressive than the OBR’s new forecast But that’s because we anticipate a stronger slowdown in inflation over the coming quarters – with an output gap closing less quickly than the OBR now projects. Households, meanwhile, look set to remain relatively cautious over the next couple of years, even as mortgage rates edge lower, limiting the recovery in households’ consumption. We expect growth of just 1.2% in 2025 and 1.4% in 2026. Further ahead, though, we agree with the OBR that the Budget measures should help lift productivity growth, but we doubt it will contribute to a 1.7% trend growth rate assumed by the fiscal watchdog.

The gilt remit – a lot to digest

Given the announcements, there has been a noteworthy increase in expected gilt issuance. For the current fiscal year this was driven by the £22bn deterioration in the cash deficit (CGNCR) to £165.1bn. Admittedly this only led to a £19.2bn increase in planned gilt sales with £3bn of that being absorbed by a planned increase in the T-bill stock. In broad-terms, markets had anticipated this scale of borrowing deterioration and this was met with a £3bn increase in planned short gilt issuance, £6bn in mediums, £9bn in longs and £3bn in index-linked, with £8.5bn left to be allocated.

However, with borrowing rising further over the forecast horizon, the estimated cash deficit (and redemption profile) for future years also rose. CGNCR is now projected £22bn higher next year, £18bn the year after, followed by £21bn and £31bn. Gilt redemptions for 2026-7 were also revised materially higher by £24bn. In total, gross gilt issuance now looks set to increase by £120bn over the coming four years, compared to projections last March.

This leaves gilt issuance extremely elevated. As a percent of GDP, gilt sales this year are estimated to total 5.6% of GDP. However, allowing for the fact that the BoE is also running down its gilt holdings with passive maturities and active sale, the net effect is closer to 9% of GDP – a level of supply that is comparable to 2008-09.

Market reaction – weighing firmer growth vs more borrowing

Given the importance of this Budget markets were always going to find a lot to take on board. From a gilt perspective, markets appear to be weighing both the increase in issuance and the impact that this might have on the BoE rate outlook. 10-year gilt yields saw a knee-jerk reaction higher by 18bps, but are currently trading 12bps higher at 4.34%. 2-year gilt yields, which we would suggest are likely to be more rate outlook than issuance sensitive, rose by 15bps to 4.31% at the time of writing. However, markets also appear to have taken on board some of the Chancellor’s growth centric approach – admittedly at the time of writing the FTSE 100 was broadly flat, however, the more domestic-economy focused FTSE 250 index initially jumped 1.8% although is currently 0.5% higher.

In terms of the overall market assessment this should in no way be compared to the disastrous mini-Budget delivered under Liz Truss’s short reign in 2022. On that day, gilt yields jumped 33bps and went on to rise by 100bps over the next three sessions. While the current gilt reaction is not comparable, the reaction of sterling is more telling. In 2022, sterling fell 2.0% to the euro and 3.6% to the US dollar. Today sterling has remained flat to the Euro (at a relatively solid £0.835) and has risen 0.4% to the US dollar to $1.301.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.