Hedging inflation: Fundamentals and scarcity

- 26 Julio 2024 (7 min de lectura)

Long-term savings need to grow more than inflation to meet future liabilities or lifestyle choices. Rapid increases in inflation – like in 2021 – make it hard to preserve real wealth in the short term, especially as interest rates tend to rise. Yet over the long term, inflation protection can be achieved through exposure to equities, credit assets and gold. In the wake of the recent inflation spike, risk premiums are high in rates and corporates have managed to maintain profit margins. On the assumption that developed market inflation reverts to close to 2%, real returns look to be healthy going forward. The one caveat is that in the US, market indices are distorted by high valuations in the technology sector and other growth stocks. That could mean a period of negative returns but not because of inflation. Over the last quarter of a century, the equal-weighted S&P 500 has delivered the same inflation-adjusted return as the market-cap-weighted index.

Price levels are higher

Despite inflation having fallen in developed economies, consumers still see unaffordable prices for consumer goods and services as one of their key concerns. Recent past increases in prices can play a role in determining inflationary expectations, which in turn can be a factor in wage demands. This is one of the residual risks in the wake of the 2021-2022 inflation shock. The consensus is that inflation in developed economies will remain above central bank targets for some time, with stickiness in service sector prices being the main reason. What happens with wages, especially in services, will determine how inflation will behave going forward and, consequently, how far central banks are able to reduce interest rates.

How consumer prices change is important for investors

The likelihood or otherwise of inflation returning close to target is important for investors. Over the last couple of years, investors have questioned which asset class has provided the best hedge against inflation. Taking the US as an example, looking at the total return performance of selected asset classes versus the US CPI index since the beginning of 2021, equities have easily been the best place to be. The S&P 500 total return index, adjusted for CPI, rose 28% over that period to the end of June. Fixed income assets lost value in real terms while gold eked out a modest positive return. At the fringe, Bitcoin had a real return of 80%.

Time horizon is important

But time horizon is vital here. In the worst of the inflation shock, between December 2020 and December 2022, everything had a negative real return. Inflation was higher than expected and higher inflation lasted longer than anyone expected. As such, ex-post, inflation risk premiums embedded in financial assets were nowhere near large enough. The reason for that is the world had just gone through two decades or more of low inflation and expectations were low. Back in the 1970s, real returns on many financial assets were negative because of unexpected increases in inflation. In the 1980s, the reverse was true. It is noteworthy, however, that even in 2021-2022, the S&P 500 had the lowest real negative decline compared to gold and fixed income assets. Despite its appeal as being an alternative to fiat money (a currency backed by a government, rather than a commodity) Bitcoin lost 49% of its real value. Since the end of 2022, equities, cash and credit have delivered positive total returns as inflation moderated and because yields had adjusted to the higher inflationary environment.

Equity returns beat most things

A long-term horizon is useful for planning asset allocations. The same exercise shows that since 1999 most core assets in the US have delivered positive real returns. Equities and gold top the table, with cash (represented by short-term Treasury bills) losing money in real terms. That reflects the aggressive cuts in interest rates following the global financial crisis, which took rates below the (low) rate of inflation.

The hierarchy of returns over that 2000-2024 period should be instructive for investors looking to achieve an appropriate portfolio allocation going forward. If inflation is to return to close to target, then it is likely that equities again will be the best performing asset class over the long term. The real total return over this period for the S&P 500 was an annualised 4.8% while an index of US Treasuries delivered just a 1.0% annualised real return. Credit and inflation-protected securities, both of which embed additional risk premiums compared to Treasuries, delivered annualised returns of 2.3% for investment grade, 3.7% for high yield and 2.3% for inflation-linked.

The profit motive helps

It is obvious why equities do better over the long run. When prices go up they feed directly into higher revenues. Companies are, of course, subject to higher costs, but they tend to respond to that to maintain positive margins where they can. Equity valuations reflect that persistence of profits (or promise of profits when it comes to some companies). There has been a political focus on the question of profiteering being a reason for the apparent persistence of inflation during the most recent shock (indeed, the European Central Bank and our own macro research team have addressed this question). However, this is just functioning capitalism (although the most egregious examples of profiteering would risk both consumer and regulatory backlashes). The downside for equity performance during inflationary episodes is higher interest rates which undercut valuations through a higher discount rate for future (and more uncertain) earnings. However, once rates have peaked and inflation begins to moderate, stocks tend to outperform.

Scarcity as a virtue

I have never paid that much attention to gold as it attracts attention from folk that are prone to believing our financial system is doomed. That is now also a philosophy associated with some Bitcoin aficionados. The inflation-proofing attraction of both is not that one will be carrying around a sack of gold coins and an encrypted cold wallet full of bitcoin to survive in a post-apocalyptic world, but because they both have scarcity. There is a finite supply of gold in the world and a lot of it is hoarded. There is also a finite amount of Bitcoin (or digital gold as some call it) that can be mined and there is a tendency to hoard it (in case some of the wilder forecasts where its dollar value might rise comes to fruition – at which point it can be sold for real money). Thus, both gold and Bitcoin appeal to some investors as inflation hedges. The problem I have with both is that some of the darker reasons put forward for investing in them have limited appeal beyond the echo chambers of the internet. Nevertheless, recognising that they have done well in relation to inflation, some modest exposure to them could be useful. Certainly, gold has tended to have an extremely low correlation with equity returns historically. It could also be that gold tends to increase before inflation, as was the case in 2020 when central banks were throwing a lot at combating the impact of COVID-19.

Inflation linked

Bonds that are linked to inflation have been around since the 1980s and have been particularly useful instruments where investors have liabilities that are also linked to inflation, like some pension funds. They function as an inflation hedge when bought at issue and held to maturity. However, during their life they are prone to volatility driven by changes in market interest rates and inflation expectations. That means over different periods, the performance of inflation-linked bonds can be quite different to the performance of inflation itself. Hence, the inferior performance of inflation-linked bonds in recent years, which reflects the balance between the impact of higher rates (negative) relative to inflation accrual (positive). Indeed, shorter-dated inflation-linked bonds did better during the last few years because of their reduced level of interest rate sensitivity. Over the long term the inflation-beating performance is good, delivering an annualised 2.3% inflation-adjusted return in the US market. As such they should be part of an inflation hedging strategy with a long-term horizon.

Careful of valuations though

The data used here is from the US but the same will apply elsewhere. One qualification around equities is the type of exposure. During 2000-2010, the S&P 500 delivered a negative total return adjusted for inflation. That was because the starting point was a very concentrated bubble in valuations at the end of the 1990s. The equally-weighted S&P 500 index fared much better over the decade, although real returns in bonds were superior. The point is that valuation matters as well as inflation protection. Over the long run that should wash out but today’s market-cap valuation in the US is extreme because of the concentration of technology stocks. That may be starting to crumble a little now. Inflation-proof portfolios built today should have a more diversified exposure to stocks, ideally with an average valuation lower than that of the market-cap S&P 500. Cash looks better now than it has done for some time because of high real interest rates but rates exposure should morph into longer duration government bonds once yield curves steepen again. Credit premiums are a healthy above-inflation source of return.

Building real wealth again

The real value of some assets has been hit by inflation and the market adjustments that were triggered. These have mostly been in the fixed income world where interest rate risk premiums were too low with hindsight. Now rates are higher with positive real rates and inflation premiums that are slightly above central bank target levels. If central banks are successful and long-term inflation expectations have not been unanchored, then real returns across fixed income assets and broader equities should potentially be positive going forward, particularly over what should constitute a longer-term horizon (three to five years).

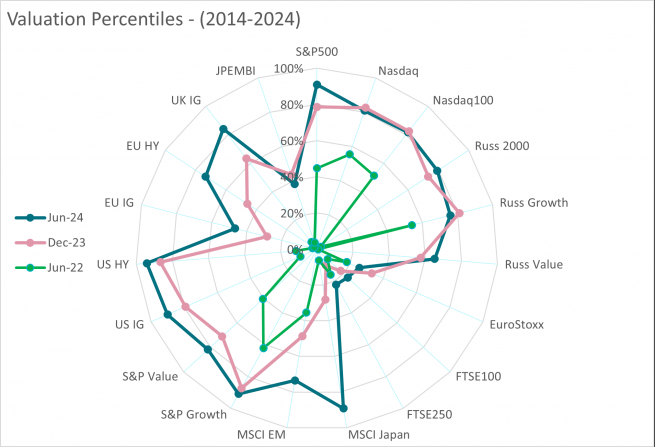

Just a last point on risk asset valuations. Since the Federal Reserve (Fed) started to increase interest rates in 2022, the valuations of US equity and credit assets have increased. I would suggest this reflects confidence among investors that the Fed would be successful in bringing inflation down and achieving a soft landing. So far, so good. However, considering there is still a record amount of money in money market funds, it is not clear what would happen if cash started to be reallocated into risk assets. Would valuations become even more stretched? Or would a meaningful reallocation only happen in response to a growth shock and following rapid cuts in rates and rapid adjustments in equity and credit valuations? As the spider chart below shows, the US is expensive (price-to-earnings ratios and credit spreads relative to a 10-year history) while the rest of the world is more soberly valued. UK and European equities and euro credit are the cheapest assets in this framework. If investors become worried, the choices seem clear.

100% = Expensive (12-month forward price-earnings ratio at peak of 10-year distribution; credit spread at narrowest of 10-year distribution)

0% = Cheap (12-month forward price-earnings ratio at trough of 10-year distribution; credit spread at widest of 10-year distribution)

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento/ material audiovisual. La información incluida en este documento/ material audiovisual se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.