US reaction: Core inflation sticky again, but eclipsed by jobless claims

- 10 Octubre 2024 (5 min de lectura)

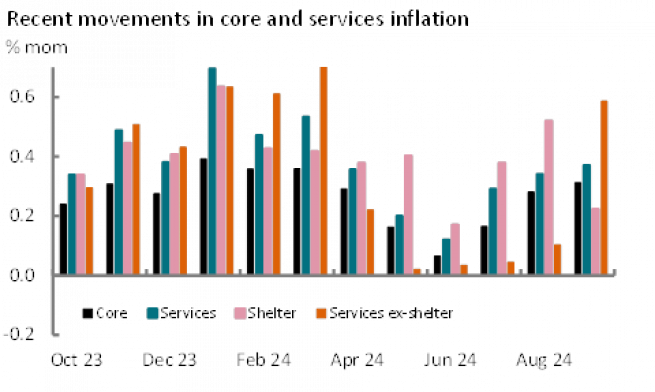

US CPI inflation came in above consensus for September, the headline rate easing to 2.4% from 2.5% in August, but firmer than the expected 2.3% (a 0.2% monthly gain compared to a 0.1% expected). Core inflation reported its second consecutive above consensus report, rising on the month by 0.3% - the same as last month (0.31% vs 0.28% unrounded) – compared to expectations for 0.2%. The core annual rate of inflation edged higher to 3.3%, back to its June level – although still a 3-year low before that.

Although the CPI miss to consensus was small in overall terms, albeit the second such for ‘core’, the details of the report add a little more caution. First, today’s inflation reading came despite a very benign month for oil prices, feeding through to gasoline prices. Gasoline fell by 4% on the month (adjusted) compared with a modest rise last year. This took 0.2% off the headline rate in September. Importantly this looks likely to unwind next month with oil prices having picked up across October, versus a sharp 4.3% drop last October. Second, the more modest impact from services inflation, which rose by 0.4% on the month and took the annual rate to 4.7% and a 32-month low, was buoyed by the weakening in shelter inflation, which gained just 0.2% on the month. This is the second weakest monthly print in 3-years and adds further evidence that an eventual slowdown in housing costs is starting to materialize (after an unusually firm 0.5% rise last month). However, from the Fed’s point of view, Fed Chair Powell had made it clear that the Fed was pretty much assuming that this was in the post, whether in the data or not. Third, what a modest services versus weak shelter inflation print means is that ex-shelter inflation spiked. This measure rose by 0.6% - in line with two of the three months at the start of the year that caused the Fed to delay the commencement of its easing cycle – in turn driven by solid gains in education and medical care costs.

In broad terms, the case for US disinflation is broadly unchanged. Headline inflation is at a 3½ year low; core still close to a three year low. This suggests space for the Fed to continue to ease the restrictiveness of policy. However, we suggest that depressed energy prices are contributing to the weakness in headline inflation – and may not persist - with core inflation still elevated by shelter inflation (4.9% y/y), which should ease, but with ex-shelter services inflation also high at 4.4%, which may not. The question then is about how quickly the Fed may ease policy. The minutes to September’s FOMC meeting stated that a ”substantial majority” supported the 50bps move. But the minutes also reported that “some” would have “preferred a 25bps reduction”, while “a few .. could have supported such a decision” and “Several .. that [25bps] would be in line with a gradual path of policy normalization”. This conveys a sense of meaningful pushback from the Committee in September. Today’s figures remind that there is likely to be some need for restrictive policy over the coming quarters to ensure that inflation returns to target on a sustained basis. With financial conditions now looser than the average of the previous decade, we argue that the Fed’s implicit endorsement of the market’s aggressive expected easing is overcooked. Indeed, following the recent payrolls print markets have repriced the outlook for Fed easing. We forecast two 25bps cuts over the next two meetings. However, we suggest that market and Fed expectations that rate cuts will continue smoothly across next year will be election dependent. We see several election scenarios, including the re-election of former President Trump, where the Fed’s space to ease policy is restricted across the course of next year.

Market reaction, however, was dominated by the sharp jump in jobless claims, which rose by 33k to 258k – the most in more than a year. Much of this we believe to reflect disruption from hurricane Helene, but the report also identified a rise in Michigan lay-offs, which is likely in part reflecting reduced shifts at Stellantis. Jobless claims could be elevated for a number of weeks reflecting ongoing hurricane disruption and this is likely to keep the market and Fed cautious. Markets halved the previous probability of the Fed not cutting in November, now seeing just a 16% chance of no move, and increased the likelihood of two 0.25% cuts this year to 80%. 2-year US Treasury yields dropped 6bps to 3.98% and 10-year fell by 2bps to 4.07% - although still the highest levels since end-July. The dollar dropped 0.2% against a basket of currencies, but also remains at its firmest since early August.

Artículos relacionados

Ver todos los artículos

UK reaction: Wage growth hot, but broadly in line with MPC expectations

- por

- 14 Mayo 2024 (3 min de lectura)

UK reaction: UK exits recession with better-than-expected GDP growth

- por

- 10 Mayo 2024 (3 min de lectura)

EM Latin America reaction: Mexico keeps policy rate on hold at 11%

- por

- 09 Mayo 2024 (3 min de lectura)

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.