UK reaction: Looser labour market conditions point to further cut

- 15 Octubre 2024 (3 min de lectura)

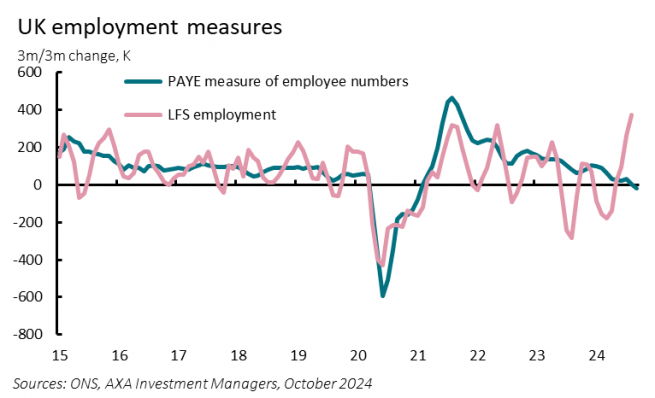

The latest labour market data point to an additional cut at the Bank of England’s meeting in November. The Labour Force Survey data showed a chunky 373K increase in employment in the three months to August and the unemployment rate edged down again to 4.0%, lower than in the previous three months and the level this time last year. Ongoing sampling issues, however, mean the data are unreliable and should be taken with a large pinch of salt. Note the survey reached an average of 88.5K individuals with a response rate to 42.8% (around 38k respondents), whereas in H1 2024, those figures were 53.1K and 17.6% (around 9k respondents), respectively.

Other measures continue to point to looser conditions. The number of vacancies, for instance, fell for the 27th consecutive period in the three months to September. And the PAYE measure of employee numbers was broadly unchanged in September – it fell by 15K on the month – after a drop of 35K in August, the largest since the early stages of the pandemic. The ONS also noted that year-over-year growth in both the Workforce Jobs – a measure based on business surveys – and the PAYE measures has slowed significantly over the past 18 months or so. The KPMG/REC Report on Jobs survey, meanwhile, suggested that some firms were putting hiring decisions on pause until after the Budget on October 30th, due to concerns over potential tax changes.

Likely most important for the BoE, though, will be the ongoing deceleration in wage growth. Average weekly earnings ex. bonuses fell to 4.9% - its slowest pace since June 2022 – from 5.1% in the three months to July, driven by declines in both public and private sector pay regular pay; the former slowed to 5.2%, from 5.7%, and the latter to 4.8%, from 5%. Total earnings – which include bonuses – fell further to 3.8% - over a three-and-a-half-year low - from 4.1%, though the disparity largely reflected base effects, given NHS workers and civil service workers were given one-off bonus payments across the summer in 2023. On a 3-m annualised basis, total earnings grew by 2.7% and ex-bonus payments by 4.4%.

On balance, the latest labour market data should convince a majority of MPC members in November that enough slack is developing to support a gradual deceleration in wage growth back to more sustainable levels over the next year or so. Note the BoE’s Decision Maker Panel survey showing businesses expect wage growth to be around 4% in 12 months’ time. In addition, we expect a renewed decline in CPI inflation in September – released tomorrow morning – to 1.8%, with services CPI inflation slowing to 5.1%. Both point to one further cut in Bank Rate in November. Further ahead, the key risk remains the Budget; if the Chancellor tightens fiscal policy materially in order to close the so-called fiscal “black hole” then the BoE may be forced to tighten more aggressively to offset the hit to growth.

Artículos relacionados

Ver todos los artículos

China reaction: LNY seasonal volatility, divergent pressures

- por

- 11 Marzo 2024 (3 min de lectura)

ECB: Towards a (very) informed first rate cut in June

- por François Cabau,

- 07 Marzo 2024 (5 min de lectura)

China reaction: 5% GDP growth target does not erase concerns over deflation

- por

- 05 Marzo 2024 (3 min de lectura)

ECB Preview: Rate cut pondering, decision likely in June

- por François Cabau,

- 01 Marzo 2024 (3 min de lectura)

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.