ECB update: Cautiously surfing the dovish wave

- 07 Octubre 2024 (3 min de lectura)

Little doubts of a 25bps rate cut in October

The September flash inflation print highlighted significant downside to ECB’s forecasts unveiled just a few weeks before. Crucially, core inflation came at 2.7% y/y in Q3 24 while ECB’s forecasts revised in September had 2.9% y/y. Given the surprise came from core components, the downside is likely to transpire at least through a few quarters. In our reaction to the print, we thought it was enough for the ECB to decide on 25bps rate cut in October (no rate cut expected previously at that meeting), also since President Lagarde expressed increased confidence in the timely return of inflation to target in her statement at the European Parliament. Such comments were also echoed by historically hawkish ECB board member Isabel Schnabel, while she also highlighted growth headwinds and softening labour demand, making clear the lack of willingness to fight market pricing which had over 90% probability a 25bps rate cut at the next meeting.

Weak domestic demand with little hope of (imminent) significant pick-up

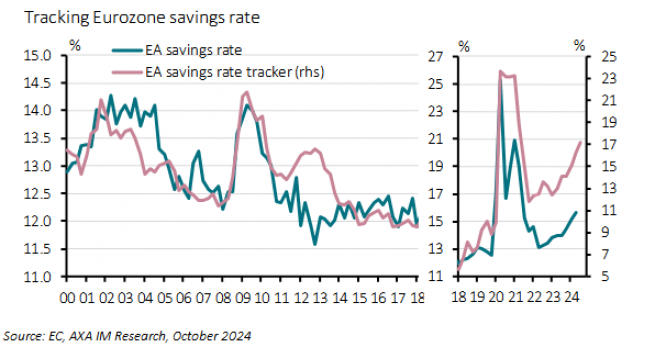

Euro area final domestic demand (aggregated private and public consumption and overall investment) contracted in Q1 and Q2 this year. While this was mainly led by investment, private consumption growth was anaemic, growing by an average 0.1% q/q in H1 24 – and contracting in Q2, despite significant real purchasing power gains. Latest business and consumer confidence surveys are consistent with our view of no imminent material domestic demand pick-up by contrast with ECB’s latest forecasts. We think that softening labour market, significant political uncertainty in Germany and France, and decent real deposit rates are likely to maintain household’s savings rate high, as suggested by our tracker (Exhibit 1), and delay the investment recovery. Downward revisions in these two countries in our latest global macro monthlywere the main driver for lower, still below consensus, euro area 2025 GDP growth forecast at 0.9% (consensus & ECB: 1.3%).

Our latest inflation forecast update shows ECB’s inflation target undershooting for most of 2025

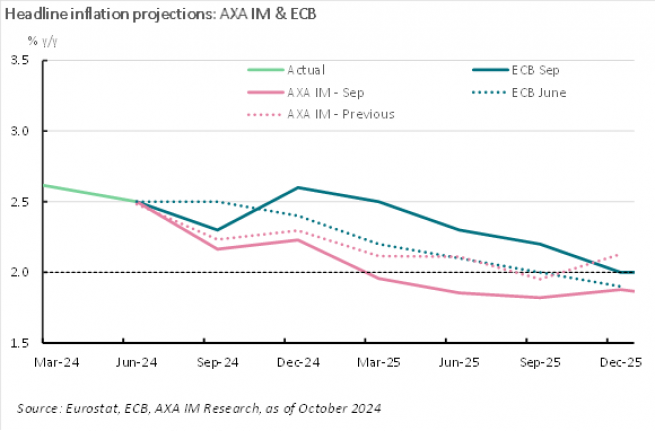

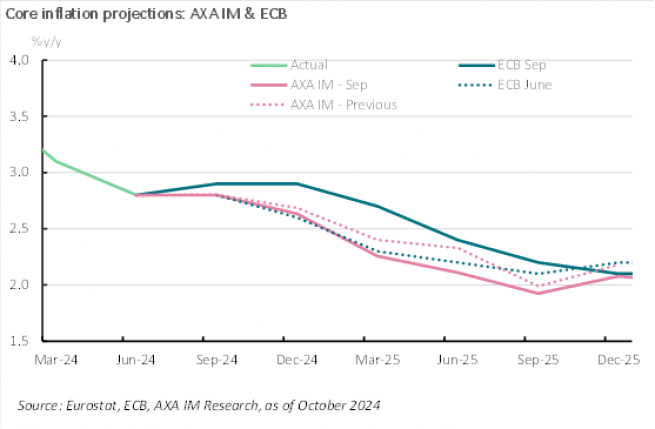

Beyond the abovementioned September inflation print, ECB’s 2025 inflation forecasts look too high. Exhibit 2&3 show similar difference between ours and ECB’s projections for headline and core inflation, implying that oil price assumptions play a likely minor role. Reflecting uninspiring domestic demand prospects, marked by the services-led consumption rotation running out of fuel - we have abated services (and goods) price seasonality. We now forecast headline inflation to come below ECB’s 2% target in the first three quarters of 2025, reaching a low in Q3 25 (1.8% y/y), while core inflation would continue its downtrend without too many humps and bumps.

We now expect back-to-back 25bps depo rate cuts through H1 25 to 2%, with a skew to the downside

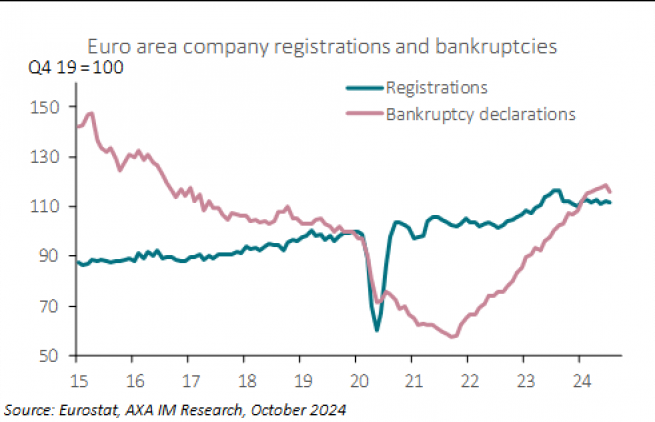

With already minimal deviation of actual inflation to ECB’s target, we think disappointing activity momentum will eventually lead the ECB towards a more forward-leaning policy bias, putting less – though unlikely to fully disappear - weight on its triptic (wage, productivity, unit labour cost) and justifying a step-up in ECB easing its restrictive stance from its quarterly forecast meetings – our expectation since September 2023. While our revised nominal policy rate would be within the vicinity of neutral by-end H1 25, it would be significantly more restrictive than in the previous fifteen years. As such, we cannot rule out the ECB going with a more aggressive easing cycle, either going 50bps in December or continuing for longer its easing cycle depending on data, but also on other central banks’ behaviour. Although euro area inflation sensitivity to euro currency tends to be small, the ECB will have to be mindful of its relative monetary policy stance, cautiously surfing the current overwhelming monetary policy easing narrative across all major advanced economies. Finally, Covid-19 and the 2022 inflation shock and their associated policy response have likely extended a growth cycle that started in mid-2013 that has yet to rollover. Although not an imminent concern, there is a significant net destruction of companies (Exhibit 4) in the euro area while fiscal leeway is very limited to non-existent across member states.

Artículos relacionados

Ver todos los artículos

UK reaction: June cut remains firmly on the cards

- por

- 09 Mayo 2024 (3 min de lectura)

US reaction: Fed unmoved on rates, tapers QT

- por

- 02 Mayo 2024 (3 min de lectura)

Eurozone data wrap-up: Path beyond June ECB rate cut remains uncertain

- por François Cabau,

- 30 Abril 2024 (3 min de lectura)

Japan reaction: Cautious stance from the BoJ

- por

- 26 Abril 2024 (3 min de lectura)

US reaction: Growth slows further, but inflation sting in the tail

- por

- 25 Abril 2024 (3 min de lectura)

UK reaction: Unemployment rises but the focus remains firmly on pay growth

- por

- 16 Abril 2024 (3 min de lectura)

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.