US Outlook – Second Term Trump

- 04 Diciembre 2024 (5 min de lectura)

KEY POINTS

A new chapter

The US expanded by 2.8% annualised in Q3 2024 with consumption seeing a strong 3.7% rise. Although this followed weak headline expansion in Q1, due to dips in consumer and government spending as well as exports, Q2 was a robust 3.0% and 2024 as a whole looks set to deliver growth of 2.8%. However, despite growth’s robust pace, CPI inflation fell to 2.6% in October, around the pace consistent with the Federal Reserve’s (Fed) 2% PCE inflation target and marginally lower than we had anticipated last year (we forecast 2.9% for 2024 now, compared with 3.2% one year ago).

This combination of stronger growth and softer inflation largely reflected improving supply conditions: global supply chain tensions eased; labour market efficiencies improved, with vacancies falling more than unemployment has risen; and the labour supply increased, primarily from strong immigration. This has allowed the Fed to ease policy more quickly than expected and we expect one further 0.25% policy rate cut before year-end to leave the Fed Funds target at 4.25-4.50% as the Fed appears on track to delivering a soft landing.

Policy uncertainty replaces political uncertainty

If 2024 has played out a combination of recent years’ economic shocks and the Fed’s policy management, the coming years look more likely to be driven by the new administration’s policy direction. November’s election will return former President Donald Trump to the White House in 2025, with majorities in both houses of Congress. This was the result we expected1 , although the final outcome was less close than polls suggested (Exhibit 5). This avoided prolonged election outcome uncertainty but substituted political uncertainty for policy uncertainty. Trump campaigned on policies of fiscal easing and deregulation, which should support growth, but he also campaigned for tighter migration restrictions, trade tariff increases and made several geopolitical statements, which could all have a materially detrimental impact on the growth outlook. Yet for now there is significant uncertainty about the scale of implementation, with the immediate market reaction playing down some of the more growth-restricting policies.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cuYXhhLWltLmNvbS9pbnZlc3RtZW50LWluc3RpdHV0ZS9tYXJrZXQtdmlld3MvdXMtMjAyNC1wcmVzaWRlbnRpYWwtZWxlY3Rpb24tcHJldmlldy10cnVtcC1mYWNlcy1uZXctYWR2ZXJzYXJ5Ij5QYWdlLCBELiwg4oCcVVMgMjAyNCBQcmVzaWRlbnRpYWwgRWxlY3Rpb24gUHJldmlldzogVHJ1bXAgZmFjZXMgbmV3IGFkdmVyc2FyeeKAnSwgQVhBIElNIE1hY3JvIFJlc2VhcmNoLCAyNiBKdWx5IDIwMjQuPC9hPg==

We are cautious of the growth outlook. Trump’s signature fiscal easing is likely to include a $4bn+ cost to extend the 2017 household tax cuts due to expire at the end of 2025. While the expiry would present a marked fiscal cliff, extending them merely maintains the status quo – it is not a stimulus. Corporate tax cuts to 15% (from 21%) would be different but even these are only small at 0.2% of GDP and previous tax cuts have rarely been shown to boost investment. Deregulation might prove more of a boost, particularly in gas production. But more broadly deregulation, which might extend to tech, AI and banking, typically provides moderate tailwinds, rather than one-off boosts. Even if the proposed Department of Government Efficiency does lift productivity (rather than just cut spending), this is unlikely to materialise in the first two years.

More fundamentally, further immigration restrictions and deportations would constitute a supply shock – limiting, or reversing labour supply growth – as would tariffs. Both are to be implemented to an uncertain scale but both would reduce US trend growth rates and boost inflation.

Two further uncertainties could also impair growth. While a full Budget is far from being prepared, the scale of tax cuts suggested is likely to see the deficit rise from its already elevated pace of around 6% of GDP per annum over the next 10 years. The Congressional Budget Office (CBO) currently estimates US debt exceeding 120% of GDP by 2034 and this could rise closer to 130% after Trump’s policies. This risks markets driving yields higher to incorporate a credit premium over coming years, with key risks if CBO deficits deteriorate further and the Treasury increases coupon issuance. Any such rise in yields would be a further headwind.

We are also mindful of geopolitical developments. Changing policies for Ukraine, the Middle East and increased economic tensions with China could topple the current, delicate geopolitical balance. We could not tell what new equilibrium might emerge but we are mindful that financial markets are rarely keen on uncertainty surrounding such transitions, something which may also dampen the growth outlook.

Growth to slow, inflation to rise

Our forecast is that with US activity enjoying solid momentum for now and a further loosening in financial conditions – in part in response to Trump’s win – the economy should post another solid year in 2025 and we forecast growth of 2.3%. However, as we expect the new administration to introduce growth restraining policies soon after inauguration, we expect growth to slow markedly across 2026, to leave annual growth at 1.5%, and annualised H2 2026 growth slower still.

Amid policy uncertainties, risks to our forecasts are two-sided. Growth could be supported beyond our expectations by a government efficiency drive, or a deregulatory spur to activity. But we do not assume full implementation of Trump’s supply shocks, which could impact the economy more. We are also wary of a rebalancing of geopolitical risks and the impact on financial conditions and growth.

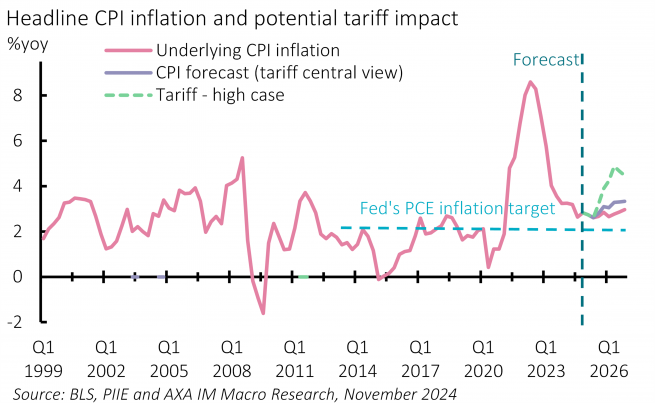

While there is much debate over the growth outlook, we see fewer reservations over the outlook for inflation. The combination of boosting demand conditions and simultaneously restricting supply seems inevitable to deliver higher inflation. The question is again one of extent, given uncertainties surrounding the scale of policy implementation. The Peterson Institute estimates2 if Trump delivered the full extent of his campaign rhetoric, inflation could rise by up to 7ppt in 2025. We do not expect full implementation – although concede uncertainty. We also consider dollar strength as likely to dampen the inflation impact at the margin, as may increased oil and gas supply by lowering energy prices. We forecast inflation to edge lower to 2.8% on average in 2025 but forecast 3.2% for 2026 (Exhibit 6). These forecasts are consistent with the Fed’s PCE inflation target measure remaining above target over the coming years.

Less space for monetary policy easing

We consider these developments likely to restrict the Fed’s space for monetary loosening, certainly relative to its September projections that saw the median (upper bound) Fed Funds forecast at 3.50% by end-2025 and 3.00% by end-2026. Indeed, we consider the Fed’s aggressive initial policy easing to have reflected a rebalancing of risks, trading off reduced downside growth/upside unemployment risks now for modestly above target inflation in the future. We still expect the Fed to ease policy to 4.50% by end-2024, but then consider just one more cut in 2025 to 4.25% in March, before supply shock policies raise the Fed’s inflation outlook. Longer term, based on our assessment that growth will start to slow in 2026, we expect the Fed to cut rates to 3.50% by end-2026. However, our expectation for the near term is for government policy to limit the Fed’s easing cycle. We also expect the Fed to end its quantitative tightening programme in the latter half of 2025.

There are wider concerns over the Fed’s independence under Trump. Both the President and Vice President-elect have suggested the President should have some say over policy. But recently Trump has said he does not want to mandate Fed actions but simply wants the right to comment on them. Trump has also suggested he would let Fed Chair Jerome Powell serve his term until 15 May 2026. This should allay concerns that Trump would remove Powell – something we suggest is legally trickier than it sounds. However, the Fed may still feel Trump’s ire if it ends its easing cycle in response to government policy.

- TWNLaWJiaW4sIFcuLCBIb2dhbiwgTS4gYW5kIE5vbGFuZCwgTS4sIOKAnFRoZSBpbnRlcm5hdGlvbmFsIGVjb25vbWljIGltcGxpY2F0aW9ucyBvZiBhIHNlY29uZCBUcnVtcCBQcmVzaWRlbmN54oCdLCBQZXRlcnNvbiBJbnN0aXR1dGUgZm9yIEludGVybmF0aW9uYWwgRWNvbm9taWNzLCBTZXB0IDIwMjQu

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.