Japan Outlook – Further hikes on the cards in 2025, but 2026 will mark the end

- 04 Diciembre 2024 (5 min de lectura)

KEY POINTS

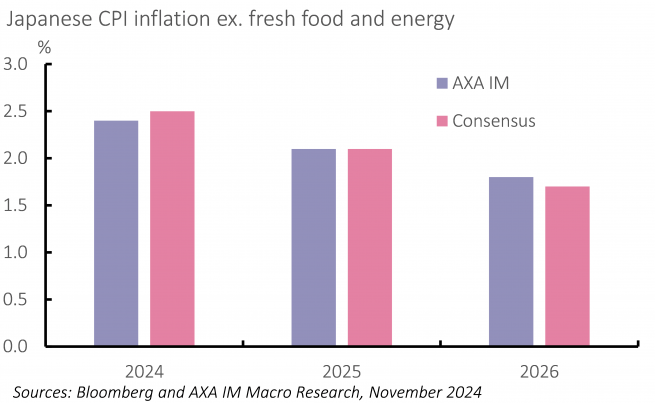

Japan appears to have closed the door on deflation in 2024, with a virtuous wage/price spiral appearing to take hold. Indeed, the 2024 Shunto wage negotiations resulted in a 3.6% increase in base pay and a 5.17% rise in total pay, well above the average of the previous 10 years – 0.9% and 2.6%, respectively. Businesses also showed they were willing to pass on higher costs. While the headline inflation rate bumped about throughout the year due to the removal and reimposition of energy subsidies, the underlying inflation rate – which excludes fresh food and energy – is on course to average 2.4% this year (Exhibit 11). Prices in the labour-intensive services basket also showed signs of picking up.

A similar result likely will emerge next year, with Rengo – the key union – setting its target for total pay at 5% for large firms and “over 6%” for small and medium businesses. While the slowdown in inflation across 2024 means the risks lay to the downside for this settlement, we see scope for a structural rise in wages over the coming years. Dwindling labour supply amid an ageing population should increase bargaining power, while rising inflation expectations among households and businesses should pave the way for larger pay rises in the coming years. We look for a rise in base pay of around 3% in 2025 and 2026. With wage gains staying elevated, growth above trend and the yen staying around the ¥150-mark, underlying inflation looks set to average 2.1% next year. More generally, though, estimates suggest that consistent 3% pay rises each year – feasible given labour supply constraints are unlikely to abate soon – are probably consistent with underlying inflation of just below 2%. Combined with expectations of an appreciating yen in 2026, this means CPI inflation excluding fresh food and energy will likely ease to a little below target at 1.8% in 2026.

Japan’s economy is on course to decline by 0.3% over 2024 as a whole. Factory shutdowns in the auto sector due to concerns over safety signoffs weighed heavily on Q1 growth and inventories and net trade knocked 0.2 percentage points (ppt) and 0.6ppt off quarterly growth in Q2 and Q3, respectively. After a weak start, household spending has started to ramp up, helped by a rebound in real incomes, while strong growth in corporate profits has supported an increase in capex.

Looking ahead, the new government’s ¥39tn fiscal package will underpin just around a 0.6% increase in government expenditure in 2025. The expected income tax threshold increase and minimum wage should support a further modest recovery in private consumption. Note, though, that growth in household spending will be limited by weak confidence; at least some of the real income increase will most likely be saved. A further increase in profits, meanwhile, as nominal GDP growth remains on an upward path, and the growing need to invest in technology to replace a declining workforce will keep investment ticking over. Yet, our expectation of a material slowdown in the US in 2026 would hit net trade, while higher borrowing costs would lead to a slowdown in private investment and consumption. We look for growth of 1.1% in 2025, before slowing to 0.9% in 2026.

With the virtuous wage/price spiral broadly embedded and growth slightly above trend in 2025, we expect the Bank of Japan (BoJ) to maintain its policy normalisation path, with 25 basis point hikes in December this year and September 2025, after Upper House elections in July. But we think the BoJ will be forced to halt policy normalisation there. With tariffs and reduced labour supply expected to lead to a material slowdown in the US in 2026 and the Federal Reserve beginning to ease policy again, pressure on the yen looks set to reverse, putting downward pressure on inflation in the medium term, while slowing growth will muddy the domestic picture. We think the BoJ will maintain its key policy rate at 0.75% throughout 2026.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.