It could be a tweet

- 31 Enero 2025 (3 min de lectura)

Economic expansion typically sees equity multiples rise and profit margins grow. This should then translate into strong total returns for equity investors. The current US economic expansion is 18 quarters strong - the S&P 500 has delivered a total return of 100% from the end of the second quarter (Q2) in 2020 to the end of 2024. The threats to this continuing are multiple – the end game for technology firm super-profits, a recession, or interest rate hikes. Or it could simply be a tweet from the White House. If the consensus on the macroeconomic backdrop, Federal Reserve (Fed) policy, and that artificial intelligence (AI) still has legs are all correct, the bull market should carry on. But if a trade war is triggered, all bets are off and fixed income will be the likely winner.

Buffering

The US equity market wobble caused by the release of DeepSeek, a new Chinese AI model, has been relatively short-lived. As of market close on Thursday 30 January, the S&P 500 was just 0.78% off its all-time high while the technology-heavy Nasdaq index was just over 2.4% lower. Investors are still digesting what the release of DeepSeek’s model will mean for the AI supply chain, and particularly for the prospect of continued massive capital spending on powerful semiconductors, data centres and dedicated sources of energy. In turn there are questions around the ability of large US technology companies to continue to keep generating supernormal profits if it turns out training and running open-source AI models can be done more cheaply. However, encouraged by technology company results and the (largely) welcoming comments about the importance of advancements in the science, the conclusion has been that AI is here to stay as a major theme for equity investors (and for the broader economic outlook). While there are always winners and losers in periods of rapid technological change (remember Netscape anyone?), the emergence of cheaper, more efficient AI means more rapid and widespread adoption through the economy and for a growing number of applications. We are still going to need lots of chips, data centres and power.

Cash machines still delivering

Equity bears will have been encouraged by how quickly some of the technology companies’ stock prices fell at the beginning of last week. The argument being that the performance of US equities has been concentrated in a handful of large technology companies and if the era of super-profits for them is over, then the market overall will correct in terms of valuations and in terms of earnings growth expectations. We will see, but for now the big guys are reporting strong numbers. Microsoft, Meta, and Apple reported earnings per share numbers that were significantly above year earlier levels. Based on the 21 technology companies in the S&P 500 universe which have already reported calendar Q4 2024 earnings so far, sales growth has been 7.6% and earnings growth11.5% - according to aggregated data from Bloomberg. DeepSeek’s methodology has already been incorporated into incumbent AI platforms and the pipeline of model development is likely to see even quicker and more powerful models being released (my technology colleagues in the equity team point to the upcoming release of Google’s Gemini Flash Thinking 2.0 model). Cheaper, more powerful AI models may be a threat, but they also are an opportunity for the AI revolution to reach further, faster.

The cycle still in favour

I, like lots of others, have questioned US equity valuations. Thinking broadly about the market, a trigger for a significant adjustment in market levels needs to come from either an external shock, a growth slowdown, or an increase in interest rates. Looking at data covering several decades, some trends are clear. When the US economy is expanding (i.e. not in a recession as defined by the National Bureau of Economic Research) there tends to be an expansion of profit margins which generates a rise in earnings per share. There also tends to be an expansion of price-earnings multiples. So, if there is economic growth, earnings tend to rise, and investors are happy to pay a higher price to benefit from those rising earnings. Rising earnings and rising multiples mean positive total returns.

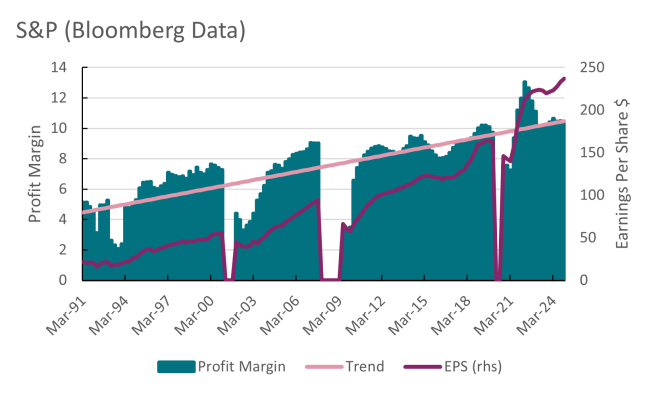

The chart below shows the evolution of the aggregate profit margin, its estimated trend and earnings per share for the S&P 500 since 1991. I have taken out recession periods. Margins rise during expansions. Since 2023, the Bloomberg data suggests the aggregate profit margin for the S&P 500 has been above 10%. For the Information Technology sector, margins have been above 20% and have been rising.

Concentration

A note of caution here. The same analysis on the equally weighted S&P 500 shows a declining profit margin since 2022 even though earnings have continued to rise. If technology company margins were to decline, then the market cap-weighted data for the market would obviously look much worse. On a more optimistic note, maybe Donald Trump’s deregulation drive and lower corporate tax cuts will help non-technology companies boost their own profit margins.

Exceptions

Multiples tend to increase during expansions. The most recent exceptions were in the period following the bursting of the dot.com bubble in the early 2000s and, briefly, during the most recent Fed tightening period. As I showed recently with the Shiller price-earnings (P/E) analysis, the market reached very high valuations in 1999 and what followed was a multi-year re-adjustment of equity valuations to much lower levels. Between 2000 and 2008, the broader market multiple halved. In the Fed tightening period, the multiple fell by around 40%.

Positive but tempered returns

From a macroeconomic perspective, we don’t anticipate a recession in 2025 and expect the Fed to remain on hold. The slightly more hawkish message from Fed Chair Jerome Powell this week was that there was no urgency to reduce rates, but a rate hike is not really on the cards now, unless the flow of data changes materially. So, with continued expansion and no rate hike, the odds are that the market continues to benefit from the earnings backdrop and multiples staying at, or slightly above, current levels. However, beating the S&P 500’s 25% total return in 2024 looks a stretch. Even if the 14% expected growth rate in earnings is achieved, the P/E multiple would need to go up by two to three points.

Hello bonds

As always, we need to watch bonds. Over the last year, the 10-year US Treasury yield has remained within the 4% to 5% range, apart from that period last summer when the Fed thought the labour market was slowing. All the concerns about a Trump-driven inflation surge, or a fiscal crisis, have not yet manifested themselves in bond prices. But should yields rise, this will be a problem for equities, especially if it reflects a change in the market’s view on Fed policy. My default view is that if bond yields rise and that causes stocks to fall, buy bonds.

Now, Mr President…

At the global level, profit margins have been expanding. This is impressive considering the rise in costs experienced in the wake of the pandemic. Data based on the Euro Stoxx and Japan’s Nikkei index suggest a steady increase in margins in the past couple of years. Global stock market returns have been well founded. Continued performance has some challenges; the expansion runs out of steam; US technology sector earnings expectations start to weaken; the rates outlook changes because of the materialisation of US inflation risks; bond yields rise; or Trump’s policy agenda hits business and investor confidence. There is some expectation that the coming weekend will see Trump announce tariffs on major trading partners. There are no good outcomes from this direction of travel. The world has waited for his trade policy but when it comes it could be the straw that breaks the camel’s back.

(Performance data/data sources: LSEG Workspace DataStream, Bloomberg, AXA IM, as of 30 January 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2025. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.