US reaction: CPI provides some reality check

- 11 Septiembre 2024 (5 min de lectura)

KEY POINTS

US CPI August headline inflation rose by 0.2% on the month, in line with expectations, seeing the annual rate fall to 2.5% its slowest pace since February 2021. However, core inflation rose by a faster than expected 0.3% on the month (0.28%), marginally above the expected 0.2%, although the annual rate remained unchanged at 3.2% (unadjusted) as expected.

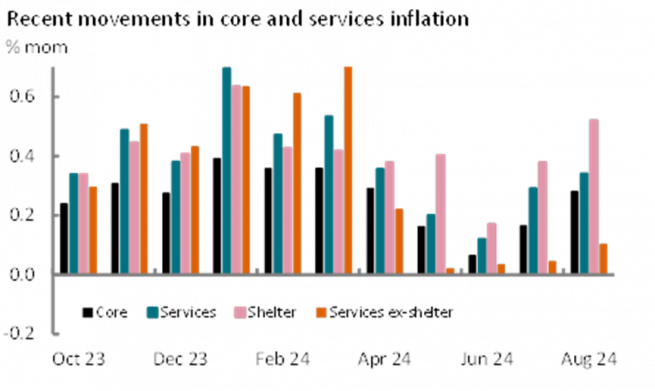

In broad terms, goods price inflation continued to slow, -0.2% on the month and the same as the average pace of decline seen since June 2023. The annual pace of goods decline was -1.2% and its joint lowest since the start of the pandemic. Energy also continued to fall, including through household energy and motor fuel costs. This had the biggest impact on headline inflation compared to the rise in August last year. But overall services inflation accelerated for the second consecutive month to +0.34% having spent two months averaging half that pace in May and June. Services inflation accelerated because of a modest pick-up in ex-shelter inflation (Exhibit 2), which we had considered likely after three months’ of effective stagnation. And a rise in shelter inflation to 0.5% (its highest since the abhorrent January reading), which in turn reflected a rise in owner equivalent rents (OER), which also picked up to 0.5%, its highest since January. By contrast, rents on primary residences settled in at the pace it has averaged since last December. August’s reading is likely to be another erratic spike in OER, with the longer-term typically underpinned by primary rents, which in turn we also expect to ease further. The annual rate of services inflation eased to 4.8% - a 2½ year low.

Exhibit 1 illustrates the two drivers of inflation. Core inflation has softened in trend terms over recent months largely reflecting the softening in ex-shelter services inflation, although the latest reading suggests that this disinflation may be coming to an end. Headline inflation has fallen more sharply thanks to the sharp negative contribution from energy, something that will be exaggerated further in September, but beyond which risks reversing somewhat. In broad terms we remain confident that inflation is coming down and forecast inflation to average 3.0% this year and 2.6% next – consistent with PCE inflation reaching the 2% target sustainably next year. We still expect some deceleration in shelter inflation over the coming quarters and this should offset what we expect to be a less negative contribution from goods and energy inflation in Q4 2024. However, we do not consider inflation to be on track to sustainably undershoot the inflation target. Indeed, we think that the Fed still has a job to do in ensuring a softening in the economy sufficient to achieve a return to target. As such, we consider the scale of Fed cuts currently priced by markets as excessive. We continue to forecast the Fed will start to lower rates by 0.25% next week and continue to see only one further cut this year in December (although acknowledge a risk of a November cut). We do not envisage 100bps of cuts this year as markets. We consider the outlook for next year as election dependent, but stress that a Trump win would likely limit the Fed to two cuts next year if the next administration enacts the demand stimulus and supply restrictive policies Trump suggests.

Market reaction was sharp to today’s 0.03ppt upside beat to core inflation, but to our minds reflected the excessive pricing seen since payrolls, including the acceleration in average earnings to 0.4% on the month in that report. The perceived chances of a 50bp rate cut in September dropped to just over 10% from around 25%, whereas the chances of 125bp of cuts by year-end reduced to just over 10% from 43% before the release. 2-year Treasury yields rose by 7bps to 3.64% - although still a 2-year low; 10-year yields rose 4bps to 3.66% (a 16-month low). The dollar also rose by 0.3% against a basket of currencies, but this is now 1.1% higher than its end-August lows.

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.