Canada Outlook – reducing spare capacity

KEY POINTS

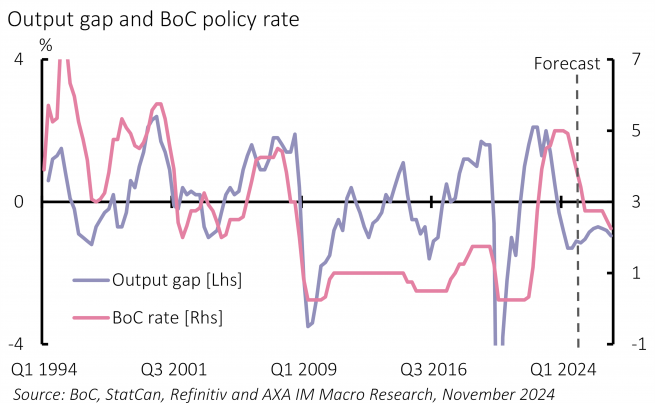

Canada’s GDP looks set to rise by 1.1% in 2024, in line with our view since April but quicker than forecast a year ago. Inflation has fallen faster with the headline at 2.0% and the core median rate at 2.4% – above target but much closer than we expected a year ago. This allowed the Bank of Canada (BoC) to ease policy faster than expected; it is forecast to end 2024 with a final 0.50% cut in its policy rate to 3.25%, 100 basis points (bp) more than we anticipated a year ago. The BoC estimates an output gap that reached 1.3% of GDP by mid-2024 as subdued growth fell short of a potential rate it estimates between 2.1-2.8%. It sees this adding disinflationary pressure. The BoC has been easing policy closer to neutral (estimated 1.75-2.75%) to close the gap and anchor inflation around target (Exhibit 10).

A number of factors should help narrow the output gap across 2025. First, we forecast growth to accelerate next year. There is some evidence the fast pace of BoC easing has underpinned a revival in consumer confidence and started to firm retail activity. Indeed, with the fading impact of the mortgage rate increase into 2025, the BoC’s cuts should soften the mortgage conditions headwind, while more subdued inflation should firm real disposable income growth. We remain cautious about business and residential investment outlooks. Yet we now forecast GDP growth accelerating to 2.1% in 2025.

This would not close the output gap alone but the BoC estimated a slowdown in potential growth to 1.1-2.4% in 2025 as temporary migrant workers fall and a more recent restriction to target 1.1m total migration between 2025-2027 should slow it further. Alongside our own weaker productivity estimates, these suggest potential growth towards the lower end of the BoC’s range, indicating less excess supply and tempering cuts. Inflation has fallen faster than we forecast reflecting globally familiar combinations of improved supply conditions, labour matching and energy markets. Inflation is on track to average 2.4% in 2024, but we expect this to fall further into next year, to average 1.7%, before rising to 1.9% in 2026.

As such we expect the BoC’s enthusiasm for policy cuts to fade early next year. We forecast the BoC to slow cuts to a 0.25% clip in early and expect it to stop cutting at the upper end of its neutral rate assessment – at 2.75% in March – as it recognises improvement in activity following its prompt easing, wary of the lags in monetary policy.

External developments are likely to be key, none more so than the US elections. The new US administration is likely to see a series of measures that further restrict the BoC’s space to ease policy further. US tariffs, which we expect to exclude Canada, should further boost spillovers of persistent solid US GDP growth into 2025. Moreover, a weaker Canadian dollar – currently around 20-year lows – should limit BoC divergence from the Federal Reserve.

Canada also faces its own election. While Prime Minister Justin Trudeau’s minority Liberal government could fall earlier, an election must be held by October 2025. Current polling suggests right-of-centre Conservatives led by Pierre Poilievre would emerge as the new government. Parties have not published manifestos but concerns about social spending would make a shift in the tax and spend balance likely, which could add headwinds to the 2026 growth outlook.

We expect growth momentum to soften in 2026, largely on the back of a slowing US economy and we forecast Canadian GDP growth of 1.7%. An externally led slowdown, with the economy still exhibiting spare capacity is likely to prompt the BoC to resume easing and we expect the policy rate to close 2026 at 2.25%.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

AXA IM y BNP Paribas AM están fusionándose y reorganizando progresivamente nuestras entidades legales para crear una estructura unificada.

AXA Investment Managers se unió al Grupo BNP Paribas en julio de 2025. Tras la fusión de AXA Investment Managers Paris con BNP PARIBAS ASSET MANAGEMENT Europe y sus respectivas sociedades holding el 31 de diciembre de 2025, la nueva compañía ahora opera bajo la marca BNP PARIBAS ASSET MANAGEMENT Europe.