US reaction: Fed reacts to short-run data with jumbo cut

- 18 Septiembre 2024 (5 min de lectura)

The Fed began its rate easing cycle with a 0.50% rate cut taking the Fed Funds Rate to 5.00-4.75%. This easing defied guidance from Fed officials before the purdah period, which had discussed “moderate”, “gradual” and “cautious” easing of policy restrictiveness and both our own and consensus forecasts that had all looked for a more gradual start to the easing cycle of 0.25%. However, with the Fed appearing to use recognized ‘back-channel’ communications of stories to the Wall Street Journal, markets had begun to suspect in recent days that a bigger easing was on the cards. One member voted against the Committee decision for a 50bps cut, instead voting for a 0.25% reduction.

The Fed’s accompanying statement spelt out a gradual evolution in thinking. It continued to note that the economy was expanding at a “solid pace”, but did note that employment growth had “slowed” (as opposed to moderated) and that inflation had “made further progress towards” its inflation objective, with risks now “roughly in balance”, as opposed to moving into “better balance”. The statement also stated that when “considering additional adjustments” (previously this had been when considering “any adjustments”) showing that the Fed considered this the start of an easing process.

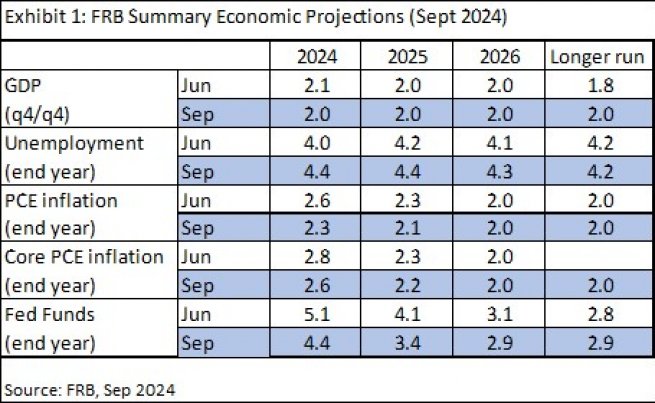

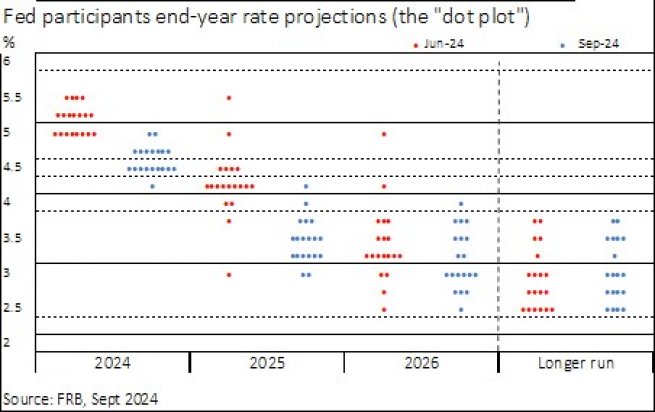

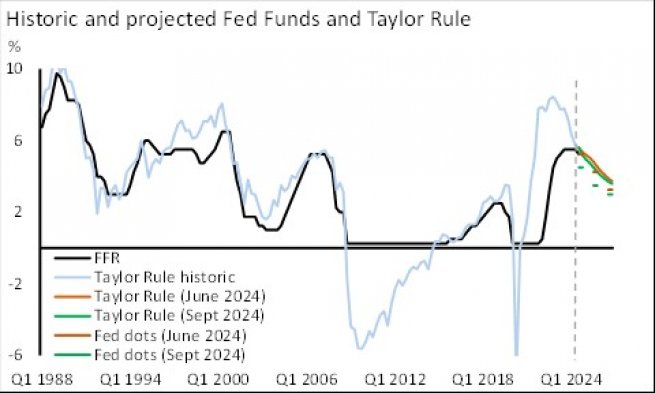

This outlook for lower rates was clearly spelt out in the Fed’s quarterly Summary of Economic Projections (SEP) (Exhibit 1). Following today’s 50bp cut, the SEP showed median Fed forecasts for two more 25bps cuts this year (to 4.5-4.25%) (November and December) and then four 25bps cuts across 2025 to 3.5-3.25% (with two projected for 2026) (Exhibit 2). This came with modest underlying economic forecasts. GDP forecasts were largely unchanged at 2.0% (although the Fed raised its trend pace of growth, lifting it to 2.0% from 1.8%). The unemployment forecast was revised higher to 4.4% for this year and next (from 4.0% and 4.2%). And inflation was revised lower for this year to 2.3% from 2.6% (2.6% from 2.8% for core) for this year and 2.1% from 2.3% (2.2% from 2.3% for core) for next. Exhibit 3 illustrates that the scale of Fed rate projection adjustments was far more than the inferred policy prescription changes using the Fed’s economic projections

The Fed Chair’s press conference addressed the sharp change in the Fed’s outlook, including the unusual practice outside of recession of beginning an easing cycle with a 50bps cut. He cited the two payrolls reports, which had shown a dip in payrolls and rise in the unemployment rate, which the Fed had not been expecting. He also repeatedly mentioned the revisions process to payrolls for Mar 23 – Mar 24, stating that the Fed was “mentally adjusting” current numbers with that in mind. And he said that the decision had been made in part on a “risk management” basis, rather than purely an economic outlook. Powell did, however, suggest that we should not look at “this [50bps cut] and think that this is the new pace”. Indeed, the Fed Chair provided little justification for why the Fed had cut by 50bps, other than his overriding assessment that the US economy “was in a good place and today’s decision was about trying to keep it there”.

Fed Chair Powell suggested that in terms of the outlook a good place to start was the SEP outlook. However, the last 13 weeks has shown that as an unreliable guide at best. In June, 11 of 19 members thought there would be one cut this year at most, today only two members think the Fed are done and 10 look for at least two more (0.25%) cuts (100bps in total). We ourselves had seen the shift in Fed’s reaction function and had recently been expecting three cuts to 4.75-4.50%, by year-end. However, following today’s 50bp we now expect two more 0.25% cuts to 4.50-4.25%. However, we recognize the Fed’s recent reactivity to short-term data as a risk to that view. The Chair explained that future decisions would be based on the evolution of data and stated decisions to speed up or slowdown the pace of tightening would be taken in the light of upcoming employment data. However, it is this reactivity to short-term data that saw the Fed eschew gradual easing over recent months when other central banks began to ease and now have seen a jumbo first cut. By contrast, the Bank of England for example is reverting to anticipating future economic activity. Fed Chair Powell today said that the Fed “can’t look a year ahead and know what the economy is going to be doing”. This is a problem for an inflation targeting central bank. We assume a more gradual approach going forwards, but upcoming Fed moves will be subject to the natural volatility in the data.

Beyond this year, the Fed appears to take little account of the election cycle. To our minds, this could have a meaningful impact on the Fed’s space to ease policy. A precise forecast will thus only be possible after the election outcome is known later this year. We continue to suggest that a either a Trump win, or some of Harris’ proposed policies will make it difficult for the Fed to ease policy as much as they suggest by end-2025 and we suggest that if the Fed continues to ease policy at this pace without signs of economic slowdown, it risks having to reverse policy over its forecast horizon.

With markets a little over 50/50 in anticipating the size of today’s easing, there was some room for catch-up. Markets increased the chance of another 75bps of easing by year-end to 70%, from 30% before the meeting and 2-year yields yields fell sharply initially, but are currently down just 2bps at 3.62%. 10-year yields however rose a touch by 3bps to 3.71% respectively. The dollar also dropped by 0.6% immediately after the announcement, but subsequently recovered all of this loss.

Artículos relacionados

Ver todos los artículos

China reaction: GDP as expected, questions raised on policy direction

- por

- 18 Enero 2024 (5 min de lectura)

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2024. Todos los derechos reservados.

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.